Dealing with delayed customer payments can be a significant challenge for businesses, especially in industries where extending credit terms is a norm. Fortunately, accounts receivable factoring offers a practical solution by converting unpaid invoices into immediate cash, thus providing businesses with much-needed working capital.

Essentially, this financing method bypasses the lengthy wait times for customer payments, enabling companies to manage operational costs effectively. However, as exciting and valuable as this tool may sound, businesses must be aware of its particular aspects before using it.

So, in this blog, we’ll provide businesses with a comprehensive understanding of accounts receivable factoring, how it works, the different types available, and a comparison with traditional accounts receivable financing.

Moreover, we will further explore this financial strategy's benefits and potential costs. Let's explore how accounts receivable factoring can be a resourceful and flexible option for your business’s monetary requirements.

What is Accounts Receivable Factoring?

Accounts receivable factoring, often called invoice factoring, is a financial strategy where a business converts its unpaid invoices into immediate cash by selling them to a factoring company. This setup helps businesses quickly access funds, sidestepping customer payment wait times.

In a factoring transaction, three leading players are involved. They are as follows -

- Seller (Business): The company owns the unpaid invoices and wants to turn them into fast cash.

- Customer: The individual or business that owes money for goods or services received from the seller.

- Factoring Company (Factor): The third-party entity that buys the unpaid invoices at a discount and takes over collecting payments from the customer.

Two important terms to know -

- Advance Rate: The percentage of the invoice value the factoring company pays upfront to the seller, usually between 70% and 90%.

- Factoring Fees: The factoring company's charges for its services may include a discount fee for buying the invoice and a service fee for managing collections.

Factoring benefits industries like manufacturing, logistics, and construction, where extending credit terms to clients is expected. It allows businesses to quickly convert outstanding invoices into cash, manage operational costs, and maintain a stable cash flow without the hassles of getting a traditional bank loan.

Also Read: Top Long-Term Personal Loans of 2024 in The Philippines

How Does Accounts Receivable Factoring Work?

Accounts receivable factoring is a financing process where a business sells its outstanding invoices to a factoring company at a discounted rate.

This allows the business to receive immediate cash while the factoring company collects payments from the business's customers, offering a quick solution to improve cash flow and maintain operations.

Here's how it works in the Philippines -

1. Submission

The business submits unpaid invoices for services rendered or goods delivered to a factoring company. The factoring company reviews the invoices and may require verification documents.

2. Advance

After verifying the invoices, the factoring company advances a portion of the invoice value to the business. This advance generally ranges from 70% to 90% of the total invoice amount.

It is worth noting that factors like the customer's creditworthiness and the industry in which the business operates can affect this percentage.

This stage is often swift, with advances sometimes happening on the same day the invoices are submitted, giving businesses immediate cash to cover vital expenses.

3. Verification and Collection

Next, the factoring company verifies the validity and collectibility of the invoices. They might contact customers to confirm details or assess their ability to pay.

Once verified, the factoring company takes over the collection process, including handling disputes or issues. This lets business owners focus on their core activities without worrying about chasing payments.

4. Final Payment

When the customer pays the invoice in full, the factoring company releases the remaining balance to the business. This final payment is minus the factoring fees, which usually include discount and service fees.

The discount fee is a percentage of the invoice amount, while the service fee covers administrative tasks like invoicing and collections.

Also Read: Loan Table for Teachers with EastWest Bank

Types of Accounts Receivable Factoring Available in The Philippines

When exploring accounts receivable factoring, it’s crucial to understand the types available. Each offers unique benefits and risks depending on your business needs and financial situation.

Here, let us take a look at the different types of accounts receivable factoring available in the Philippines in greater detail -

1. Recourse Factoring

Recourse factoring is the most common type. The business remains responsible if the customer does not pay their invoice. Due to this liability, fees are generally lower than other factoring types.

Recourse factoring can be economical for businesses confident in their customers' reliability and payment habits. However, the downside is that if a customer defaults, the financial burden falls back onto your business.

2. Non-Recourse Factoring

In non-recourse factoring, the factoring company assumes the risk of non-payment. If the customer doesn’t pay, the factoring company absorbs the loss, not your business. This arrangement offers peace of mind, especially if your customers’ creditworthiness is uncertain.

The trade-off, however, is higher fees due to the increased risk borne by the factor. This type of factoring can significantly mitigate the risk of bad debt but will dramatically impact your profits.

3. Notification Factoring

Notification factoring involves informing your customers that their invoices have been factored in. This transparency can streamline collections as customers know payments should be directed to the factoring company.

4. Non-Notification Factoring

Non-notification factoring keeps the factoring arrangement confidential. Customers are unaware that you’ve factored their invoices, and your business continues to manage the collection process.

This is especially useful for businesses, as it helps them maintain their customer relationships and prevents any perception of financial instability from cropping up in the future.

5. Spot Factoring

Spot factoring is used for single, one-time transactions. It’s ideal for businesses needing occasional cash flow boosts without committing to a long-term arrangement. This flexibility allows enterprises to factor invoices as required, though it might come with higher per-transaction fees.

6. Regular Factoring

Regular factoring involves an ongoing arrangement with the factoring company. It provides consistent cash flow support for businesses that require regular liquidity.

Due to the sustained business relationship, this arrangement is often more cost-effective over time and can offer better terms than spot factoring.

Also Read: Top Small and Medium Enterprises in the Philippines

Get the financial support your Philippine SME needs with N90’s Fast Financing Solutions. Apply today and get potential loan approvals within 24 hours! Give your business the financial boost it needs to excel!

Accounts Receivable Factoring vs. Accounts Receivable Financing - Key Differences Between The Two Tools

Understanding the difference between accounts receivable factoring and accounts receivable financing can help you decide which option may be more suitable for your business.

Both leverage outstanding invoices to improve cash flow but operate in distinct ways. Here, take a look at how they differ from each other -

1. Ownership of Receivables

In accounts receivable factoring, the business sells its invoices to the factoring company, which takes ownership of the receivables and assumes responsibility for collecting payments from customers. This means the factoring company directly manages the payment process.

In accounts receivable financing, however, the business retains ownership of its invoices and uses them as collateral to secure a loan or line of credit, continuing to manage its own collections.

2. Involvement in Collections

With factoring, the factoring company is responsible for collecting payments from customers, relieving the business of this task. This can benefit businesses that want to offload the administrative burden of collections.

In contrast, with accounts receivable financing, the company remains responsible for collecting payments from its customers, even though the receivables have been used to secure the funding.

3. Risk of Non-Payment

In factoring, especially in non-recourse agreements, the factoring company assumes the risk of non-payment if a customer defaults. This provides the business with some protection against bad debt.

In accounts receivable financing, the industry remains responsible for the repayment of the loan or line of credit, regardless of whether the customer pays, which means the business retains the risk of non-payment.

4. Impact on Customer Relationships

Factoring can sometimes affect customer relationships. Customers may become aware that their invoices have been sold to a third party, which might raise concerns about the company’s financial stability.

With accounts receivable financing, customers are typically unaware that their invoices have been used to secure funding as the business continues to handle collections and maintain direct client relationships.

5. Cost Structure

The cost of factoring is based on a fee or percentage of the total value of the invoices being factored, which can be higher depending on the customer's creditworthiness and the factoring agreement.

In accounts receivable financing, costs are typically structured as interest on the loan or line of credit, similar to traditional lending. Businesses with strong credit may secure lower financing rates than factoring fees.

Also Read: Low Interest Rate Personal Loans: What They Mean for Borrowers

Benefits of Accounts Receivable Factoring in The Philippines

Let's explore how accounts receivable factoring can be a game-changer for businesses. Here, take a look at the key benefits of accounts receivable factoring for firms in the Philippines -

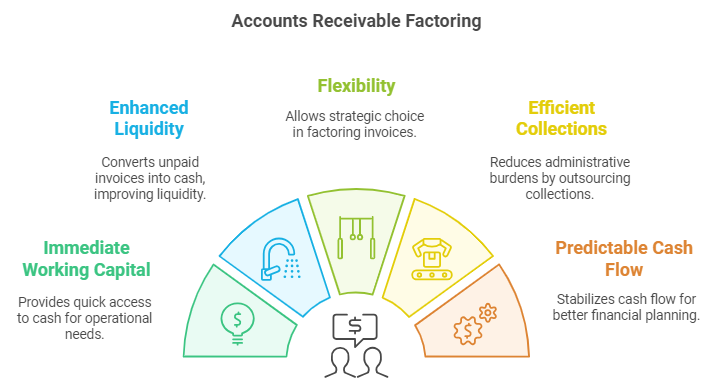

1. Immediate Working Capital

One of the most significant advantages of accounts receivable factoring is the quick access to cash. When businesses sell their invoices to a factoring company, they get a cash advance, usually between 80% and 90% of the invoice value, almost immediately.

This immediate cash flow can help cover operational expenses, meet payroll, and fund new projects without waiting for customers to pay their invoices.

2. Enhanced Liquidity

Factoring improves a business's liquidity by converting unpaid invoices into cash. This helps manage operational expenses more efficiently and avoids cash flow bottlenecks, ensuring the company can meet its financial commitments on time.

Better liquidity also means the company is more prepared to seize growth opportunities and invest in expansion.

3. Flexibility

A significant feature of accounts receivable factoring is its flexibility. Businesses can choose which invoices to factor in, allowing them to manage their cash flow strategically.

This means you can factor in high-value invoices or those from slow-paying customers, optimizing cash flow while controlling customer relationships.

4. Efficient Collections

Factoring companies take over collections, reducing administrative burdens and freeing up your business to focus on growth. Their professional approach maintains positive customer relationships.

5. Predictable Cash Flow

Factoring provides a reliable source of funds, helping businesses stabilize their cash flow. This predictability makes financial planning easier and enables better decision-making regarding investments, staffing, and other critical areas.

6. No Debt Accumulation

Unlike traditional loans, factoring keeps your balance sheet free of additional debt. It is the sale of an asset (the invoice), not a loan, so there are no monthly principal or interest payments to worry about.

This non-debt financing approach lowers the financial burden and preserves your credit lines for other needs.

7. Scalability

Factoring grows with your business. As your accounts receivable increase, the amount of financing available through factoring can also increase. This scalability makes it an ideal solution for businesses experiencing growth, allowing them to adjust their funding as their needs evolve.

Did you know that accounts receivable factoring is commonly used by small businesses in the Philippines, potentially saving them from insolvency? Check out this detailed Reddit thread to learn more.

Also Read: Applying for DTI Loans in the Philippines for Small Businesses

Cons of Accounts Receivable Factoring in The Philippines

Accounts receivable factoring can be a game-changer for businesses, but like any financial solution, it also has potential downsides.

Here, take a look at the potential cons of utilizing account receivables factoring in the Philippines -

1. Potential Impact on Customer Relationships

One downside is the potential impact on customer relationships. When you use a factoring company, they often take over collecting customer payments. This can sometimes create friction if customers are uncomfortable dealing with a third party.

2. Higher Costs Compared to Traditional Financing Options

Factoring typically has higher costs than traditional financing options like bank loans. Fees can add up and eat into profit margins. Although it provides immediate cash, the expense may outweigh the benefits for some businesses.

3. Limited to Solving Cash Flow Issues from Slow-Paying Clients

Factoring is primarily helpful in addressing cash flow issues resulting from slow-paying clients. If your business faces broader financial challenges unrelated to receivables, factoring might not be the ideal solution.

Also Read: MSME Loan Guide for Startups and New Businesses

Costs Associated with Accounts Receivable Factoring in Philippines

Understanding the associated costs is crucial when it comes to accounts receivable factoring. The fee structure can be complex, but breaking it down makes it easier to comprehend.

Let's look at the typical costs you might encounter with accounts receivable factoring -

1. Factoring Fees

Factoring companies typically charge a fee of 1% to 5% of the invoice value for their services. This fee often covers services such as collections and credit checks.

The exact cost is usually influenced by several factors, including the risk involved in collecting payments, the industry, the creditworthiness of your customers, and the volume of invoices being factored.

More extended payment periods from your customers can also result in higher fees.

2. Advance Rates

Another critical component of factoring is the advance rate, which generally ranges from 70% to 90% of the invoice value. If you have an invoice of PHP 5.6 million, you might receive between PHP 3.9 million and PHP 5 million upfront. The remaining amount is held back as a reserve and released after the customer pays the invoice.

The advance rate you receive can also be influenced by factors like the creditworthiness of your business and its customers and the specifics of your industry.

Conclusion

Accounts receivable factoring is a valuable financial tool for businesses seeking immediate cash flow by selling their unpaid invoices to a factoring company. It allows businesses to access funds without waiting for customer payments, improving liquidity and supporting day-to-day operations.

Moreover, it offers flexibility and especially benefits businesses facing cash flow gaps. Hence, it is fair to conclude that most Philippine companies can effectively utilize this solution to maintain smooth financial operations, invest in growth, and manage working capital efficiently.

They can do so by carefully understanding how it works through selling receivables, fee structures, and the relationship with factoring companies.

Frequently Asked Questions (FAQs)

1. How does account receivable factoring work?

Accounts receivable factoring works by a business selling its unpaid invoices to a factoring company at a discount. The business receives immediate cash while the factoring company takes over collecting customer payments.

The factor charges a fee or percentage of the invoice value, offering a quick solution for improving cash flow and managing operational expenses.

2. What is the step-by-step process for accounts receivable?

The step-by-step process of accounts receivable factoring is as follows -

- Submit Invoices: The business submits its unpaid invoices to the factoring company.

- Approval: The factor reviews the creditworthiness of the business’s customers and approves the invoices.

- Advance Payment: The factoring company advances a percentage of the invoice value, typically 70-90%, to the business.

- Collection: The factor collects the full payment directly from the customers when the invoices are due.

- Final Payment: Once the customers pay, the factoring company sends the remaining balance to the business minus factoring fees.

3. What is the interest rate for accounts receivable factoring in the Philippines?

In the Philippines, the interest rate or factoring fee for accounts receivable factoring typically ranges from 1% to 5% of the invoice value per month, depending on factors like the customer's creditworthiness, the invoice amount, and the agreed terms.

Some factoring companies may also charge additional service fees, so it is important to review all costs before proceeding.

4. What are the three reasons why a company may sell its receivables to another company?

A company may sell its receivables to another company for these reasons -

- Improve Cash Flow: Selling receivables provides immediate cash to cover operational expenses or fund growth.

- Avoid Collection Risks: Transferring receivables reduces the risk of non-payment from customers.

- Streamline Operations: Outsourcing collections to a factoring company allows the business to focus on core activities rather than managing outstanding invoices.