Long-term personal loans can be a viable solution for managing significant financial obligations, particularly when funds are needed for important life events or substantial expenses.

However, understanding the benefits and drawbacks is crucial for making the right financial decision. This is primarily because, without the correct financial information, you’ll not only pay more interest but also not get the loan amount your business truly deserves.

So, to help Filipinos find the best personal loans available in the country, this article will discuss the essential aspects of long-term personal loans, compare them with short-term options, and highlight their unique features.

Moreover, we'll explore some leading loan providers' pros, cons, and important details and offer practical advice on choosing and qualifying for the correct loan term that perfectly aligns with your needs.

Additionally, loan repayments are also an essential part of the loan, so it is vital to know the effective strategies to implement for a seamless loan repayment process. So, without much ado, let us look at all the critical details.

What Are Long-Term Personal Loans, And What Are Their Key Features?

Long-term personal loans are a type of financial product that allows borrowers to repay borrowed amounts over an extended period, often several years to more than a decade.

Unlike short-term options, long-term personal loans typically have fixed interest rates, ensuring that monthly payments remain consistent.

Common Uses For Long-Term Personal Loans

These loans are beneficial in situations requiring substantial financial resources -

- Debt Consolidation: Combining multiple high-interest debts into one manageable loan with a lower interest rate.

- Home Improvement: Financing significant renovations or expansions to your home, adding value in the process.

- Medical Bills: Covering large, often unexpected medical expenses, from surgeries to ongoing treatments.

Comparing Long-Term and Short-Term Loans

- Repayment Period: Long-term loans offer repayment terms extending several years, unlike short-term loans that must be repaid within a few months to two years.

- Interest Rates: Long-term personal loans typically have lower interest rates. While this means lower monthly payments, the total interest paid over the loan's life may be higher.

- Loan Amounts: Long-term options usually offer higher loan amounts, making them more suitable for significant financial needs.

Also Read: Applying for a Safe and Legit Personal Loan Online in the Philippines

Pros of Long-Term Personal Loans in The Philippines

Long-term personal loans can be an innovative financial solution for many people. Here are some of the key advantages -

1. Lower Monthly Payments

Due to the extended repayment period, long-term personal loans offer smaller monthly payments, making them more manageable for individuals with limited cash flow.

2. Larger Loan Amounts

Long-term loans allow borrowers to access more significant loan amounts, which can be helpful for major expenses like home improvements, medical bills, or business investments.

3. Improved Cash Flow Management

With smaller monthly payments, borrowers can free up more cash for other expenses, making it easier to manage overall finances.

4. Flexible Repayment Terms

Long-term personal loans typically offer flexible repayment terms, allowing borrowers to choose a duration that aligns with their financial situation, often ranging from 3 to 5 years or more.

5. Build a Credit History

Regular, on-time payments over a more extended period help build and improve your credit score, making you eligible for better financial products in the future.

Also Read: Successful Managed Funds and Investments in the Philippines

Cons of Long-Term Personal Loans in The Philippines

Long-term personal loans seem attractive with their lower monthly payments, but several drawbacks exist.

Here, take a look at some of the prominent ones -

1. Higher Total Interest Payments

Although monthly payments may be lower, long-term personal loans result in higher overall interest costs. The more extended the repayment period, the more interest accrues over time.

2. Extended Debt Burden

Long-term loans keep borrowers in debt for an extended period, limiting financial flexibility and making it harder to achieve other financial goals.

3. Stricter Eligibility Requirements

Lenders often impose stricter eligibility criteria for long-term loans, including higher credit scores and more extensive income documentation, making it harder for some to qualify.

4. Increased Risk of Default

With a more extended repayment period, there's a greater risk of financial instability, such as job loss or economic downturns, leading to missed payments and potential loan default.

5. Prepayment Penalties

Some lenders may charge penalties for paying off long-term loans early. This discourages borrowers from paying off the loan sooner, which could otherwise save on interest costs.

Also Read: Exploring Microfinance: Definition, Purpose, and Examples

Unlock the true potential of your Philippine SME with N90’s Fast Financing Solutions. Apply today and secure the capital you need for success! Get potential loan approvals within 24 hours and help push your Philippine business toward success. Avail Now!

5 Best Long Term Personal Loans Available in The Philippines And Their Features

When considering a long-term personal loan, it's essential to understand the distinct features each lender offers to find the best fit for your financial situation.

Here’s a closer look at some of the leading options available in 2024 -

1. UnionBank Personal Loan

- Loan amount: Up to PHP 2 million

- Minimum annual income: PHP 250k

- Monthly add-on interest rate: 1.29%

- Loan terms: 12 to 60 months

- Best For: Foreign residents or entrepreneurs in the Philippines

2. Metrobank Personal Loan

- Loan amount: PHP 20k to PHP 1 million

- Minimum annual income: PHP 350k

- Monthly interest rate: 1.25% to 1.75%

- Loan terms: Up to 36 months

- Best For: Best bank loan provider for all kinds of emergencies

3. BPI Personal Loan

- Loan amount: PHP 20k up to PHP 2 million

- Minimum annual income: PHP 240k

- Monthly interest rate: 1.20%

- Loan terms: 12 to 36 months

- Best For: People who want loans with low interest rates

4. EasyRFC Multi-Purpose Loan

- Loan amount: PHP 10k up to PHP 3 million

- Minimum annual income: PHP 216k

- Monthly interest rate: 4%

- Loan terms: Up to 36 months

- Best For: Best online loan provider for all kinds of emergencies

5. CIMB Personal Loan

- Loan amount: PHP 30k to PHP 1 million

- Minimum annual income: PHP 180k

- Monthly interest rate: 1.12% to 1.95%

- Loan terms: 12 to 60 months

- Best For: Best for people who want an online loan provider offering quick approvals

Also Read: Understanding the Features, Importance, and How Microfinance Works

How To Select The Best Long Term Personal Loan - Key Points To Consider Before Applying

Selecting the correct personal loan term involves a delicate balance between monthly payments and total interest paid. This balance is essential if you want to save money in the long run and manage your monthly budget effectively.

Monthly Payments vs. Total Interest

- Longer Loan Terms: Opting for a loan term of 5-7 years reduces your monthly payments, making them easier to handle. However, the trade-off is higher total interest over time.

- Shorter Loan Terms: A 2-3 years term might mean higher monthly payments, but you’ll pay less in total interest. Though demanding in the short term, this option saves you money on interest overall.

Examples of Different Loan Terms and Their Impacts

Let's look at some concrete examples to understand how loan terms affect payments and interest.

Short-Term Loan

- Loan Amount: PHP 564k

- Loan Term: 2 years

- Interest Rate: 12%

- Monthly Payment: PHP 26k

- Total Interest Paid: PHP 63k

Here, you’re paying a significant monthly amount, but your total interest is relatively low.

Long-Term Loan

- Loan Amount: PHP 564k

- Loan Term: 5 years

- Interest Rate: 12%

- Monthly Payment: PHP 12k

- Total Interest Paid: PHP 155k

In this case, your monthly payment is lower, but you end up paying more in total interest.

Consideration of Loan Amount and Repayment Ability

The loan amount and your capacity to repay it are critical factors:

- Loan Amount: Bigger loans naturally mean higher monthly payments and more total interest. Carefully assess how much you actually need to avoid borrowing more than necessary.

- Repayment Ability: Make sure the monthly payments are comfortable for you and fit within your budget. The goal is to find a repayment plan that’s both manageable and cost-effective.

Do you still need to learn how to apply for a credible low-interest personal loan worth PHP 1.5 million in the Philippines? Here, check out this Reddit post. In this post, people discuss whether an individual can avail of a loan of PHP 1.5 million at low interest rates.

Also Read: Getting a $100K Business Loan: Steps and Guide.

How to Qualify and Apply for Long-Term Personal Loans

Securing a long-term personal loan involves several critical steps. Understanding these steps can help you go through the process more smoothly and increase your chances of getting approved with favorable terms.

Here, check out how to qualify and apply for a long term personal loan in the Philippines -

1. Check Your Credit Score

Your credit score is pivotal in determining your eligibility for a long-term personal loan. It affects the interest rates and terms lenders will offer you.

A higher credit score of 700 and above can grant you access to better loan conditions and lower interest rates, leading to more manageable monthly payments and less interest over the life of the loan.

Before you apply, obtain a copy of your credit report and check for any errors or areas for improvement. Fix any inaccuracies and work on boosting your score if necessary.

2. Research Lending Options on The Personal Loan Marketplace

To find the best personal loan offers, utilize online marketplaces. These platforms allow you to receive offers from multiple lenders, helping you compare and select the best deal tailored to your credit profile and loan requirements.

3. Comparing Offers Based on APR, Fees, and Other Key Metrics

Once you have multiple loan offers, compare them based on essential metrics like the Annual Percentage Rate (APR), fees, loan amount, and repayment terms. Look at both the total cost of the loan and the monthly payments to determine what you can afford.

Pay close attention to any origination fees, late fees, or prepayment penalties that could increase your overall cost.

4. Finalizing the Application Process

To complete your application process, you need to follow these steps -

- Gather Required Documents: Collect all necessary documents, such as proof of income, identification, and any other financial information the lender may require. Being prepared can make the application process smoother and quicker.

- Pre-Qualify: Many lenders offer a pre-qualification process that allows you to check your eligibility without a hard credit inquiry, which can affect your credit score. This can help you narrow down your options before you decide to apply fully.

- Submit Your Application: Once you’ve chosen a lender, submit your application. This step usually involves a hard credit inquiry. Make sure you provide all requested information accurately to avoid delays.

- Review Loan Conditions: Carefully read the loan terms and conditions before signing. Understand any potential penalties for early repayment or late payments. If you are an existing bank or credit union customer, inquire about relationship discounts that could reduce your interest rate.

Also Read: Best Lenders for Quick Cash Loans and Instant Same-Day Approval

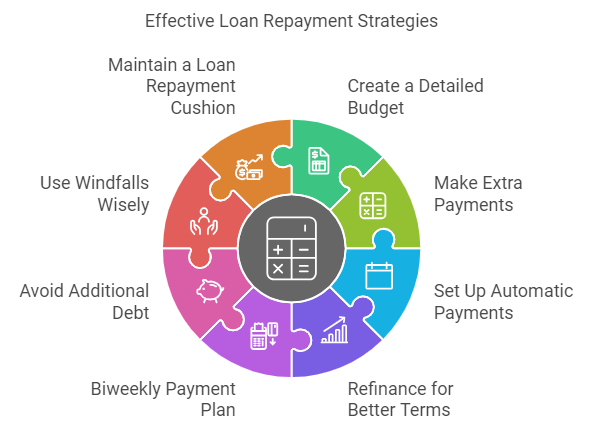

Repayment Strategies For Long-Term Personal Loans - Top Strategies For Filipino Borrowers To Implement

When you take out a long-term personal loan, it's essential to have a clear repayment strategy. This helps you save money on interest and reduces stress over time.

Here are the effective strategies to implement for a hassle-free loan repayment process -

1. Create a Detailed Budget

Establish a monthly budget that includes loan payments, essential expenses, and savings. This will help ensure that loan repayments are consistently made on time while maintaining financial stability.

2. Make Extra Payments When Possible

When possible, pay more than the minimum, such as allocating bonuses or tax refunds to the loan. Extra payments reduce the principal, shortening the loan term and lowering the overall interest paid.

3. Set Up Automatic Payments

Automating payments ensures you never miss a due date, helping you avoid late fees and protecting your credit score. This method also reduces the stress of manually managing payments.

4. Refinance for Better Terms

If interest rates drop or your credit score improves, consider refinancing your loan. This can lower your monthly payments or shorten your loan term, saving you money in the long run.

5. Biweekly Payment Plan

Instead of making monthly payments, divide your payment in half and pay every two weeks. This strategy results in one extra payment annually, reducing the principal more quickly and reducing interest costs.

6. Avoid Additional Debt

Focus on repaying your current loan before taking on additional debt. Reducing unnecessary expenses helps you allocate more funds to loan repayment and avoid becoming overburdened with financial obligations.

7. Use Windfalls Wisely

Consider using these windfalls to make lump sum payments if you receive unexpected income, such as bonuses, tax refunds, or inheritances. This can significantly reduce the loan balance and interest.

8. Maintain a Loan Repayment Cushion

Build an emergency fund to avoid missing payments due to unforeseen circumstances. Having three to six months' worth of expenses saved ensures you stay on track with loan repayments, even during financial challenges.

Conclusion

When considering long-term personal loans in the Philippines, it is crucial to keep a few key points in mind. First, research and compare multiple lenders. This involves looking at interest rates and examining loan terms, fees, and customer service quality because finding a lender that fits well with your financial needs and goals is essential.

Moreover, pre-qualifying with multiple lenders can provide you with an estimate of the loan terms and rates you might receive, and this step won’t affect your credit score. Doing so will allow you to shop around without any adverse impact.

Finally, it is vital to read reviews and check the reputation of potential lenders. A lender with positive reviews and a solid reputation can provide peace of mind, ensuring you work with a trustworthy institution.

Frequently Asked Questions (FAQs)

1. Who offers the longest-term personal loans in the Philippines?

In the Philippines, BPI, BDO Unibank, and Citi are among the banks that offer some of the longest-term personal loans, with repayment periods extending up to 5 years (60 months).

These long-term loans allow borrowers to manage their repayments, offering lower monthly payments for more significant loan amounts while maintaining competitive interest rates.

2. Can you get a 7-year Personal Loan in the Philippines?

In the Philippines, most personal loans offer repayment terms up to 5 years (60 months). Currently, 7-year personal loans are rare. However, for more extended repayment periods, you may consider other financial products like home equity loans or specialized bank offers.

Checking with banks for the latest loan options and terms is always a good idea.

3. What is the largest personal loan I can get in the Philippines?

The largest personal loan amount available in the Philippines can reach up to PHP 2 million, depending on the bank or financial institution. Lenders like BDO, BPI, and EastWest Bank offer personal loans with maximum amounts ranging between PHP 1 million to PHP 2 million.

The approved loan amount depends heavily on specific factors, such as the borrower's income, credit score, and financial capacity.

4. What rate is too high for a personal loan in the Philippines?

In the Philippines, personal loan interest rates typically range from 10% to 25% per annum. A rate above 25% is generally considered high, especially if the borrower has a good credit score and stable income.

Borrowers should compare rates from different lenders and avoid excessively high rates, which can significantly increase the overall loan cost and financial burden.