Finding immediate financial support during transitional periods can significantly challenge businesses and individuals. Bridge financing emerges as a crucial solution to this problem, acting as a temporary financial lifeline until more permanent funding is secured.

This article explores bridge financing's various facets, starting with its fundamental characteristics and eventually exploring the different types of bridge financing, their mechanics, real-life examples, pros and cons, and viable alternatives.

It is safe to say that by the end of this comprehensive blog post, you'll clearly understand how bridge financing can address your pressing financial needs and the strategic considerations involved in choosing it. So, without any more delays, let's explore bridge financing in detail.

Bridge Financing Meaning - What is it And How Does it Work?

Bridge financing is a short-term solution that meets immediate financial needs until a more permanent funding source is secured. It acts as a financial lifeline, providing quick access to cash to keep things running smoothly during transitional periods.

Bridge financing is crucial for both the real estate and business sectors. It offers short-term funding that enables quick action during critical moments.

Here, take a look at how bridge financing works in the Philippines -

1. Temporary Nature

Bridge financing is inherently short-term, generally lasting between 12 and 24 months. This interim solution quickly provides the necessary funds, helping businesses maintain momentum during critical phases of a project or business operation.

2. Higher Interest Rates

Since it's short-term, bridge financing usually has higher interest rates than traditional loans or mortgages.

For example, in early 2022, interest rates for bridge loans ranged from 7% to 9% but have increased to between 10% and 12% due to factors like the Federal Reserve’s interest rate hikes.

3. Collateral Requirements

Borrowers secure most bridge loans with collateral such as real estate or business inventory. This security reduces the lender's risk but adds a risk for the borrower, too, as there is the potential for foreclosure if the existing asset's sale falls through.

4. Flexibility in Repayment Terms

Bridge financing offers a range of repayment options. Borrowers might opt for interest-only payments, paying only the interest during the loan term and deferring the principal amount until the sale of an existing asset.

5. High Loan-to-Cost (LTC) Ratios

Lenders can offer bridge loans up to 75% LTC, covering most immediate financial needs. This makes bridge financing attractive for businesses aiming to reach critical milestones before securing long-term funding.

6. Risk Considerations

Though bridge financing provides immediate financial relief, it carries inherent risks, such as limited borrower protections and potentially higher costs due to elevated interest rates.

Borrowers must carefully assess their ability to repay these loans within a stipulated timeframe to avoid increased financial liabilities.

Also Read: Applying for a Safe and Legit Personal Loan Online in the Philippines

Types of Bridge Financing Available in The Philippines

Bridge financing comes in various flavors, each catering to different needs and circumstances. Understanding these different types can help you choose the right option in a financial crunch.

Here, let us take a look at the top bridge financing options available in the Philippines -

1. Equity Bridge Financing

Equity Bridge Financing involves exchanging capital for an equity stake in a company. This type of financing is beneficial for companies needing to cover short-term costs or fund projects before securing long-term financing.

Equity bridge financing's defining characteristic is its role in facilitating significant financial transitions for companies by providing timely capital injections.

2. Closed Bridging Loan

Due to this, closed bridging loans often offer more favorable terms and lower interest rates than their open counterparts. The lender benefits from having a precise repayment date, which reduces risk.

However, the drawback is that the borrower must comply rigorously with the repayment plan; failure to do so can lead to significant financial stress.

3. Open Bridging Loan

An Open Bridging Loan, in contrast, does not have a specified repayment date or source. This type of bridge loan is more flexible and is often used for unforeseen expenses or when immediate liquidity is needed.

Borrowers can repay the loan at any time, offering greater flexibility. However, this flexibility comes at a cost: higher interest rates and increased risk for the lender. As a result, open bridging loans can be more expensive for the borrower in the long run.

4. First Charge Bridging Loan

A First Charge Bridging Loan is characterized by the lender having the primary claim on the borrower’s property in the event of a default. Due to this priority claim, this type of loan is considered lower risk for the lender, and consequently, it often comes with lower interest rates.

The reduced underwriting risk makes it an attractive option for lenders, and the lower cost of borrowing can benefit the borrower, provided they have substantial equity in the property being used as collateral.

5. Second Charge Bridging Loan

A Second Charge Bridging Loan, on the other hand, gives the lender a secondary claim on the borrower’s property, meaning the primary lender holds the first claim in case of default. This higher level of risk translates to higher interest rates.

While this option can provide additional funds when a first-charge loan is insufficient, it comes with a significant risk premium. Borrowers should be cautious and consider their ability to manage higher interest payments in exchange for the added liquidity.

Also Read: Exploring Microfinance: Definition, Purpose, and Examples

Examples of Bridge Financing Utilized in The Philippines

Example 1: Bridge Financing Between Funding Rounds

Imagine a tech startup that has secured its Series A round of funding. This funding has allowed the startup to develop a prototype and hire initial team members. However, as the startup approaches its Series B round, it encounters unexpected delays.

They still need additional capital to cover operational expenses such as salaries, production costs, and marketing activities. In this case, a bridge loan steps in and provides the necessary funds to maintain operations until the Series B funding is secured.

This scenario highlights how bridge financing can assist companies in navigating the uncertain period between funding rounds, ensuring they maintain momentum and continue to grow.

Example 2: Real Estate Transactions

Consider a family who finds their dream home but has yet to sell their current house. A bridge loan, secured by their existing home's equity, allows them to make a down payment on the new property, ensuring they don't miss the opportunity.

This form of bridge financing is especially useful in competitive real estate markets.

Are you still unclear on the role of bridge financing in the Philippines? Check out this video. It explains in detail the role bridge financing plays in the real estate world.

Example 3: Addressing Existing Financial Obligations

In 2016, Olayan America Corp. utilized a bridge loan provided by ING Capital to purchase the iconic Sony Building in New York City. The need for immediate capital was critical to secure the deal. The bridge loan allowed Olayan to act quickly while arranging more permanent, long-term funding.

This example showcases how bridge loans can make significant business transactions possible, providing the immediate funds needed to capitalize on time-sensitive opportunities.

Other Applications of Bridge Loans in The Philippines

Bridge loans aren’t just for startups or real estate. They can be instrumental in various other instances, such as the following -

- Fix-and-Flip Projects: Real estate investors use bridge loans to finance property purchases and renovation costs for quick resale. The short-term nature of bridge loans perfectly fits the timelines of these projects.

- Purchasing Properties Off-Market: Investors looking to acquire properties from auctions or foreclosure sales can secure deals swiftly using bridge loans, which gives them an edge over competitors without immediate funds.

- Renovating Distressed Properties: Bridge loans can finance the renovation of properties already in an investor's portfolio, enhancing property value and boosting cash flow potential, particularly for those initially too risky for traditional lenders.

- Expanding Rental Portfolios: Investors can quickly expand their rental portfolios using bridge loans to finance multiple property acquisitions simultaneously. The speed and flexibility of bridge financing allow them to capitalize on lucrative opportunities and diversify their holdings effectively.

Also Read: Successful Managed Funds and Investments in the Philippines

Take control of your business’s future by applying for N90’s fast financing solutions and getting the funds you need to expand quickly! Get potential loan approvals within 24 hours to fast-track your Philippine SME towards success! Avail Now!

Pros and Cons of Utilizing Bridge Financing in The Philippines

When selecting bridge financing, it's crucial to weigh its advantages against its disadvantages to determine what fits your needs.

So, to ensure that you select the right financial tool for your immediate needs, let us explore the pros and cons of bridge financing in the Philippines -

Advantages of Bridge Financing in The Philippines

1. Quick Access to Funds

One of the biggest attractions of bridge financing is the speed at which funds can be accessed. This is particularly valuable in real estate transactions where time is of the essence.

Some lenders can approve and disburse bridge loans in as little as two weeks, allowing borrowers to move swiftly on a new property.

2. Flexibility

Bridge loans offer considerable flexibility. Payment terms are often adjustable to meet your needs, whether you want to defer payments until your current property sells or make interest-only payments.

3. Short-term Commitment

The term for bridge loans is typically short, ranging from six months to three years. This means you’re not locked into a long-term financial commitment, which can be advantageous if you plan to resolve your financial needs quickly.

4. Less Dilution Risk

For businesses, bridge loans can safeguard against dilution. By securing short-term funds through a bridge loan, you maintain control over your property or operation without giving up equity.

5. Competitive Advantage

A bridge loan can make your offer stand out in a hot real estate market. You can make a contingency-free offer on a new home, which appeals more to sellers who prefer quick and specific sales.

6. Temporary Solution

Bridge financing effectively serves as a temporary solution for homeowners needing to relocate swiftly, ensuring they have the necessary funds without immediately needing to sell their current property.

Disadvantages of Bridge Financing in The Philippines

1. Higher Interest Rates

The trade-off for the speed and flexibility of bridge financing is often higher interest rates than traditional mortgages. This increased cost can strain your financial resources.

2. Increased Debt Risk

If you’re unable to sell your existing property within the loan term, you might find yourself juggling multiple loans, heightening your debt risk.

3. Need for Collateral

Lenders typically require collateral for bridge loans, generally in the form of your current property. This means if you fail to repay the loan, you could lose that property.

4. Potential for Unfavorable Terms

Lenders may impose high fees, variable interest rates, and strict repayment conditions on bridge loans. These terms can become significantly burdensome if your financial situation doesn’t improve as expected.

5. Equity Requirements

Many lenders require significant equity in the current property, which can be a barrier for some borrowers who need more equity.

6. Financing Requirements

Some lenders may restrict borrowers by requiring them to use the same lender for their new home mortgage, thus limiting options and potentially leading to less favorable terms.

Also Read: Top Venture Capital Firms in The Philippines in 2024

Top 5 Alternatives To Bridge Financing in The Philippines

When considering financing options, it's essential to be aware of various alternatives to bridge financing. Each alternative offers unique advantages tailored to different business needs and scenarios.

Take a look at the top alternatives of bridge financing to avail instead -

1. Invoice Financing

Businesses can sell their outstanding invoices to a third-party provider through invoice financing in exchange for immediate cash. It can be handy for companies that struggle with extended payment cycles.

By converting unpaid invoices into instant cash, businesses can smooth out their cash flow and invest in growth opportunities without waiting for clients to pay their invoices.

2. Line of Credit

A line of credit provides a flexible financing option. Businesses can draw funds up to a predefined limit as needed.

Unlike bridge loans, which are typically one-time disbursements, a line of credit works more like a credit card. It offers control over borrowing and repayment, making it ideal for businesses with fluctuating cash flow needs.

3. Merchant Cash Advance

A merchant cash advance involves receiving a lump sum upfront in exchange for a fixed percentage of future credit card sales. This can be particularly advantageous for businesses that have consistent sales volumes but need quick access to funds.

It is worth noting, however, that this does not require collateral or fixed repayment schedules, which can be both a pro and a con, depending on your situation.

4. Short-term Loan

Short-term loans are appealing because they are quick to approve and disburse. They can be a lifeline for businesses that require immediate funding. However, the trade-off is generally higher interest rates than traditional loans, making them more expensive over the long term.

5. Crowdfunding

Businesses can raise funds from many people via online campaigns through crowdfunding platforms like Indiegogo's InDemand. This can be particularly effective for companies with a solid online presence or a compelling new product. Crowdfunding provides the necessary funds and helps validate market demand for your product or service.

Also Read: Getting a Loan Using Land as Collateral in the Philippines

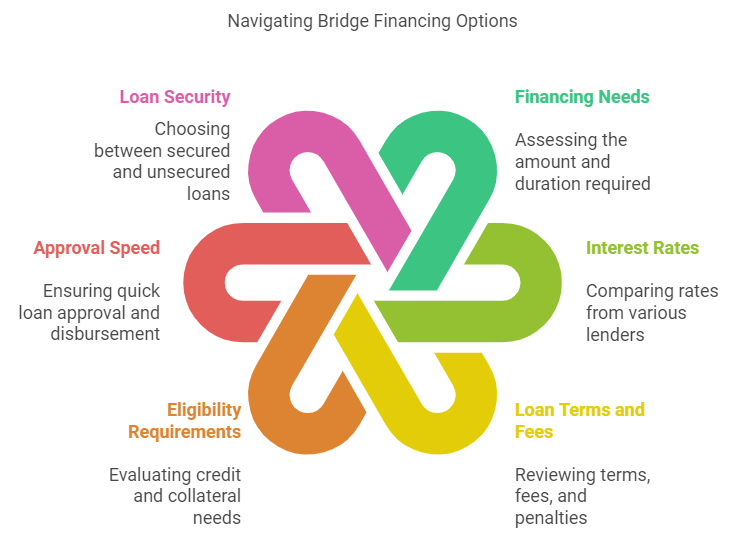

How To Select The Best Bridge Financing Option Available in The Philippines

Selecting the financial tool from the myriad of bridge financing options available can be pretty intimidating, especially for someone doing this for the first time. However, understanding each option's pros and cons and how they align with your business needs and cash flow patterns can make the decision more transparent.

Let’s dive into a comparative analysis to help you select the best bridge financing for your unique scenario -

1. Assess Your Financing Needs

Determine the exact amount and duration of financing required. Bridge financing is typically short-term, so clarify the purpose (e.g., bridging gaps in real estate, business, or cash flow needs).

2. Compare Interest Rates

Research multiple lenders, including banks, private lenders, and online platforms, to find the most competitive interest rates. A lower rate helps reduce the overall cost of borrowing.

3. Check Loan Terms and Fees

Review the loan terms, including repayment periods, processing fees, and potential penalties for early repayment. Choose a loan with terms that fit your financial situation and offer flexibility.

4. Consider Eligibility Requirements

Evaluate the eligibility criteria, such as credit score, income documentation, and collateral requirements. Select a lender whose criteria match your current financial standing.

5. Look for Quick Approval and Disbursement

Bridge financing is meant to be fast. Choose a lender known for quick loan approval and disbursement to ensure you can access funds promptly when needed.

6. Assess Loan Security (Secured vs. Unsecured)

Decide if you prefer a secured loan (requiring collateral like property) or an unsecured loan (no collateral). Secured loans typically offer lower interest rates but involve more risk if you default.

7. Read Reviews and Customer Feedback

Check customer reviews and feedback on lending platforms to ensure the lender is reliable and transparent. This can provide insights into the lender's service quality and reputation.

Conclusion

Bridge financing is a valuable tool for addressing short-term funding gaps and helping companies transition smoothly toward their long-term financial goals. However, the risks associated with bridge financing should be considered.

Firstly, companies must be aware of the potential for high interest rates and the pressure to repay on time. Mismanagement of this type of financing can lead to financial instability and impact the company's overall creditworthiness.

Moreover, strategic consideration is also crucial when opting for bridge financing in the Philippines. Companies should thoroughly understand the terms and implications before proceeding. The best way to do this is to align the structure of the bridge financing with the company’s goals and milestones to maximize its benefits while minimizing risks.

Ultimately, as we have learned from this comprehensive article, bridge financing can be a double-edged sword for Filipinos. It acts as a lifeline to bridge funding gaps and seize growth opportunities when used judiciously.

However, it cannot be understated that over-reliance on it without a clear plan can lead to financial stress. Therefore, individuals must carefully evaluate their company's ability to manage monthly payments and their confidence in meeting repayment schedules promptly.

Frequently Asked Questions (FAQs)

1. What is the difference between a bridge loan and a loan?

The main difference between a bridge loan and a regular loan is that a bridge loan is a short-term loan designed to provide temporary financing, typically for real estate or business transactions, until long-term funding is secured.

On the other hand, regular loans are long-term, with fixed terms and lower interest rates, and are used for sustained financial needs.

2. What is the core purpose of bridge funding?

The core purpose of bridge funding is to provide temporary, short-term financing to cover immediate financial needs until more permanent funding is secured.

It helps businesses or individuals manage cash flow gaps, complete transactions, or seize time-sensitive opportunities, such as purchasing property or financing operations while waiting for long-term funding or asset liquidation.

3. What are other names for bridge loans?

Other names for a bridge loan include interim financing, gap financing, and swing loan. These terms all refer to short-term loans designed to "bridge" the gap between immediate funding needs and the availability of longer-term financing.

Such loans are commonly used in real estate transactions, business expansions, or when transitioning between financial arrangements.

4. What is the period of a bridge loan?

A bridge loan typically lasts 12 months, though some may extend up to 2 years, depending on the lender and terms.

This is primarily because bridge loans are designed as short-term solutions that provide immediate financing until long-term funding is secured or an asset, like property, is sold to repay the loan.