Managing cash flow is a common challenge for businesses in the Philippines, especially for SMEs that rely heavily on timely customer payments. When faced with late fees or extended credit terms, business owners often look for financing solutions to ensure they have the necessary liquidity.

Two popular options are available in the Philippines to help with their cause: invoice factoring and invoice discounting. However, as good and effective as they are, they differ from each other in critical aspects and are, as they are tailored to meet different business needs.

So, in this blog, we will explain the differences between these two financial services in greater detail to help Philippine businesses make the right financial choice and select the one that best suits their cash flow requirements.

What is Invoice Factoring?

Invoice factoring is a financial arrangement where a business sells its unpaid invoices to a third-party company, known as a factor, at a discounted rate. In return, the factoring company provides immediate cash to the business, usually up to 80-90% of the invoice value.

The factor then takes over the responsibility of collecting payments directly from the business's customers. Once the customer pays the invoice, the factor releases the remaining balance to the company minus fees.

Invoice factoring is commonly used to improve cash flow, allowing businesses to access working capital without waiting for customer payments.

Also Read: Choosing and Registering a Dominant Business Name

Free Up Cash for Your Business Needs! Unlock the value of your unpaid invoices and stay ahead of expenses. Avail of N90’s effective invoice financing options to convert your Philippine SME’s invoices to immediate cash advances today! Apply now!

What is Invoice Discounting?

Invoice discounting is a financing method where a business uses its unpaid invoices as collateral to borrow money from a lender. The company receives a percentage of the invoice value upfront, usually 80-90%, while still retaining responsibility for collecting customer payments.

However, once the customer pays the invoice, the business repays the lender and any applicable fees or interest.

Unlike factoring, the customer is unaware of the arrangement, allowing the business to maintain control over its receivables and customer relationships. Invoice discounting is a discreet way to improve cash flow without affecting external business interactions.

Also Read: Startup Funding and Angel Investors in the Philippines

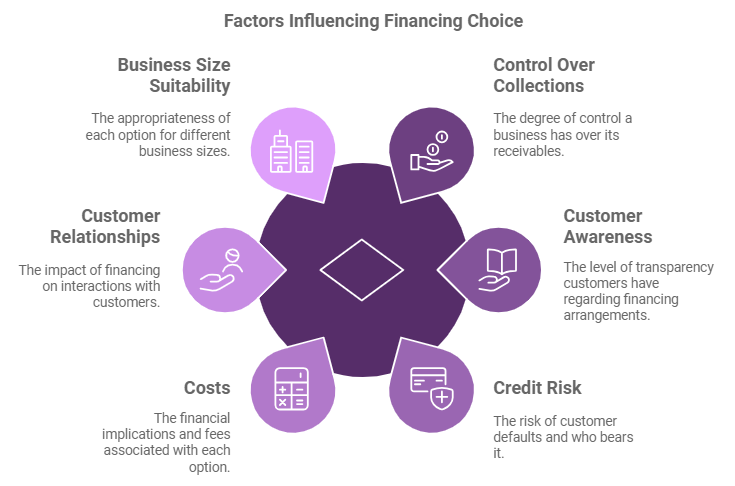

Critical Differences Between Invoice Factoring and Invoice Discounting in The Philippines

Invoice factoring and invoice discounting are two popular financing solutions that help businesses improve cash flow by leveraging unpaid invoices. While both options provide access to immediate funds, they differ significantly in terms of management, customer involvement, and control over receivables.

In the Philippines, businesses can choose between these options depending on their operational needs, customer relationships, and preferences for managing collections.

Here, take a look at the essential differences between invoice factoring and invoice discounting in the Philippines in greater detail -

1. Control Over Collections

- Invoice Factoring: In factoring, the business sells its invoices to the factoring company, which takes over collecting customer payments. This shifts the burden of managing collections to the factor, allowing the business to focus on core operations.

- Invoice Discounting: With invoice discounting, the business retains complete control of its receivables and continues to collect payments from customers. The lender provides funding based on the invoices, but the company remains responsible for following up on payments and maintaining customer relationships.

2. Customer Awareness

- Invoice Factoring: Customers are typically aware of the arrangement in factoring, as they will be instructed to pay the factoring company directly. This transparency can sometimes affect customer perceptions, signaling that the business uses external financing to manage cash flow.

- Invoice Discounting: Customers are not involved in invoice discounting arrangements. The business collects payments as usual, and the financing remains confidential. This keeps the customer unaware that the company uses its invoices as collateral for financing.

3. Who Takes on Credit Risk?

- Invoice Factoring: In non-recourse factoring, the factor assumes the credit risk, meaning that if a customer defaults on their payment, the factoring company absorbs the loss. This is beneficial for businesses looking to reduce their exposure to credit risk.

- Invoice Discounting: In invoice discounting, the business retains the credit risk. If customers fail to pay their invoices, the industry is still responsible for repaying the lender. This makes invoice discounting riskier for companies with customers with poor creditworthiness or inconsistent payment histories.

4. Potential Fees and Costs

- Invoice Factoring: Factoring companies typically charge higher fees, as they provide immediate cash flow and take on the responsibility of collections and credit risk. The cost includes the financing charge and a service fee for managing collections.

- Invoice Discounting: Invoice discounting is usually cheaper because the business continues to manage collections. The fees are primarily tied to the financing portion and are typically lower than factoring, making it a more cost-effective solution for companies that can manage their receivables.

Check out this Reddit post to learn more about the cost of factoring in your Philippine business. Here, A Redditor shares their experience in a small business using factoring. They point out that while factoring can help improve cash flow, it can be seen as an expensive and risky option.

5. Impact on Customer Relationships

- Invoice Factoring: Since customers interact directly with the factoring company for payment, the factoring company’s collection practices could negatively impact customer relationships. Hence, businesses need to choose a reputable factor to minimize this risk.

- Invoice Discounting: Invoice discounting preserves the business’s control over customer interactions, allowing it to maintain strong relationships without involving a third party in collections. This approach can help companies to avoid any potential strain on customer relationships caused by external collection agencies.

6. Suitability According To Business Size

- Invoice Factoring: Factoring is typically more suitable for small and medium-sized businesses with limited resources for managing receivables. By outsourcing collections, businesses with lean administrative teams can focus on growth without worrying about following up on payments.

- Invoice Discounting: Invoice discounting is better suited for larger, more established businesses with the resources to manage their accounts receivable efficiently. It’s ideal for companies that want quick access to cash but prefer to maintain control over collections.

7. Speed of Funding

- Invoice Factoring: Factoring can provide quicker access to cash, as the factor is motivated to collect payments and release the remaining balance as soon as possible. Factoring companies often disburse funds within 24 to 48 hours of approving the invoices.

- Invoice Discounting: Invoice discounting also offers fast access to funds, but the speed of cash flow improvement depends on the business's ability to collect payments. While funds are advanced quickly based on the invoices, companies must still collect from customers to repay the lender.

8. Long-Term Costs

- Invoice Factoring: Long-term use of factoring can be expensive due to its higher fees, which include service fees and risk coverage. The recurring costs of outsourcing collections may reduce overall profitability if factoring is used continuously.

- Invoice Discounting: Since invoice discounting generally involves lower fees, it is more cost-effective for long-term financing. Businesses that manage their collections efficiently benefit from lower overall costs than factoring.

9. Flexibility and Scalability

- Invoice Factoring: Factoring provides flexibility by offering funding that grows with the business. As the volume of invoices increases, companies can factor in more invoices and access additional funds. However, the costs may also increase as more invoices are factored in.

- Invoice Discounting: Similarly, invoice discounting scales with the business. As more receivables are generated, businesses can access more funds. Invoice discounting offers greater flexibility for larger companies, especially those looking for a discreet financing option that does not involve customers.

10. Eligibility and Approval Criteria

- Invoice Factoring: Factoring companies primarily assess the creditworthiness of a business's customers, not the business itself. This makes it a good option for companies with poor credit but a reliable customer base.

- Invoice Discounting: In invoice discounting, lenders evaluate the business's and its customers' creditworthiness. This makes it more suitable for companies with solid financials and credit history, as they will likely receive better terms and rates.

Conclusion

While invoice factoring and discounting help businesses unlock cash tied up in receivables, they operate differently. So, it is fair to conclude that the choice between these two depends significantly on the specific business's need for control, customer relationships, and cost considerations.

As we have seen in the article, a third-party factor takes control of collections in factoring, which can ease administrative burdens but involves customer awareness. In contrast, invoice discounting allows businesses to control collections, keeping the arrangement confidential.

Hence, it is vital for Philippine businesses to carefully understand these distinctions to select the most appropriate financing option for their growth and liquidity requirements.

Frequently Asked Questions (FAQs)

1. What is the difference between bill discounting and invoice discounting?

The critical difference between bill discounting and invoice discounting lies in the nature of the documents involved. Bill discounting deals with bills of exchange or promissory notes, typically short-term financial instruments, whereas invoice discounting uses unpaid invoices as collateral.

Both provide immediate cash, but invoice discounting focuses on accounts receivable, while bill discounting is based on formal payment agreements.

2. What are the similarities between debt factoring and invoice discounting?

Both debt factoring and invoice discounting are forms of receivables financing that allow businesses to access immediate cash based on unpaid invoices. Using both methods, the company receives a percentage of the invoice value upfront.

Utilizing accounts receivable helps improve cash flow and manage working capital, enabling businesses to meet short-term financial needs without taking on additional debt.

3. What is an example of invoice discounting?

An example of invoice discounting is a manufacturing company that has issued several large invoices to its clients, with payment terms of 60 days. Instead of waiting for the full payment, the company approaches a lender for invoice discounting. The lender immediately advances 80% of the invoice value, allowing the company to cover operational expenses.

Once the clients pay the invoices, the company repays the lender, minus fees or interest, keeping the transaction confidential from the customers.

4. Is invoice discounting more expensive than factoring?

Invoice discounting is generally less expensive than factoring, primarily because the business retains control over collections and customer relationships in invoice discounting.

In factoring, the factoring company takes over collections and assumes more risk, which leads to higher service fees. However, the exact cost difference depends on the lender’s terms, the business’s credit profile, and the overall arrangement.