Securing a $100K business loan can be crucial for any business since it provides the capital needed to expand operations, invest in new equipment, or manage cash flow. However, obtaining such a substantial loan requires careful planning, carefully understanding the lender’s requirements, and preparing the necessary documentation.

This detailed article will help Philippine businesses secure the amount they need, in this case, a $100k business loan, whether to grow their existing business or fund a new venture. It will walk them through all the essential steps they need to follow to increase their chances of approval and ensure they select the best financing option for their needs.

Moreover, we will explore other important factors, such as the types of loans and the eligibility criteria to qualify for a $100k business loan, which Philippine businesses can utilize to confidently navigate through the loan application process. So, without further ado, let us see how you can secure a $100k business loan in the Philippines.

Types of Loans To Utilize To Get $100k Business Loans in the Philippines

Acquiring a $100K business loan in the Philippines is a significant financial decision that can help propel your business forward, but you can only attain it if you know which type of loan to apply for.

Here are the types of loans you can consider to obtain this amount -

1. Term Loans

Term loans are one of the most common ways to secure a $100K business loan, as these loans provide a lump sum amount that you repay over a fixed period, typically ranging from 1 to 5 years.

Term loans can be used for various purposes, including expansion, purchasing equipment, or refinancing existing debt. They usually come with fixed or variable interest rates, and the repayment terms are agreed upon during the loan approval process.

2. Business Lines of Credit

A business line of credit offers flexibility similar to a credit card, allowing you to borrow funds up to a pre-approved limit, in this case, $100K. You only pay interest on the amount you actually draw, making it a cost-effective option for managing cash flow, covering short-term expenses, or seizing business opportunities.

This type of loan is ideal for businesses that need ongoing access to funds without committing to a large lump sum loan from the outset.

3. SBA Loans

In the Philippines, government-backed loans, similar to SBA loans in the U.S., are available through institutions like the Department of Trade and Industry (DTI) or the Small Business Corporation (SB Corp). These loans offer favorable terms and lower interest rates, making them an attractive option for businesses seeking a $100K loan.

4. Invoice Financing

Invoice financing allows businesses to borrow money against their outstanding invoices. If your company has a significant amount of receivables, you can use them as collateral to secure a $100K loan. This option provides quick access to cash without waiting for clients to pay their invoices, making it an effective solution for improving cash flow.

5. Equipment Financing

If you need $100K to purchase or lease new equipment, equipment financing is an option where the equipment itself serves as collateral for the loan. This type of financing usually offers favorable terms and interest rates, as the risk to the lender is lower.

It is beneficial for businesses operating in industries like manufacturing, construction, or agriculture, where possessing high-cost equipment is essential for ease of operations.

Also Read: Best Short-Term Business Loans for Fast Financing

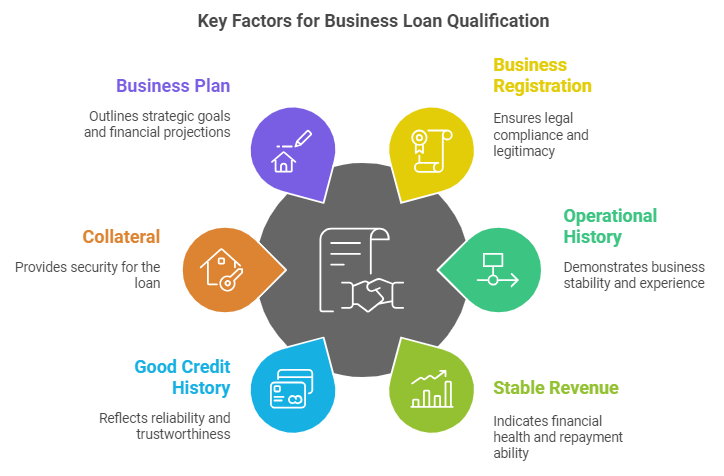

How to Qualify For a $100k Business Loan - Key Eligibility Criteria Required For Businesses in The Philippines

Qualifying for a $100K business loan in the Philippines involves meeting specific criteria related to your business’s financial health, operational history, and legal compliance.

So, to ensure that is the case, always ensure your business is well-prepared and meets certain key requirements, as these can potentially increase your chances of securing the necessary funding to support the growth and operations of your Philippine business.

Here’s a brief overview of the key requirements a business must comply with to attain a $100k business loan in the Philippines -

1. Business Registration and Legal Compliance

Your business must be legally registered and compliant with Philippine regulations. This includes having the necessary business permits, licenses, and registration with government agencies like the Department of Trade and Industry (DTI) or the Securities and Exchange Commission (SEC).

2. Operational History

Lenders typically prefer businesses that have been operational for at least one to two years. This operational history demonstrates that the business is established and capable of generating consistent revenue, which in turn reassures lenders about the business's ability to repay the loan.

3. Stable Revenue and Cash Flow

You must demonstrate a stable and sufficient revenue stream because lenders will assess your financial statements, including income statements, balance sheets, and cash flow statements, to ensure your business generates enough income to cover loan repayments.

4. Good Credit History

A solid personal and business credit history is crucial, as lenders will review your credit score to determine your creditworthiness. A high credit score indicates a reliable borrowing history, which increases your chances of loan approval and potentially allows you to secure better interest rates.

5. Collateral (if required)

Some lenders may require collateral to secure a $100K loan, especially if your business is newly established or has a limited credit history. Collateral can include real estate, equipment, or other valuable assets that the lender can claim if the loan is not repaid.

6. Solid Business Plan

A detailed and well-prepared business plan can strengthen your loan application. This plan should clearly outline your business goals, financial projections, and how the loan will be used to achieve these objectives, as lenders always look for a clear strategy that demonstrates how you plan to grow your business and repay the loan.

7. Personal Guarantee

Lenders may require a personal guarantee from the business owner, especially for large loan amounts, because a personal guarantee adds an extra layer of security for the lender.

If the business cannot repay the loan for some reason, the owner is personally responsible for repayment.

Also Read: Small Business Startup Funding for Women

Improving Approval Chances For a $100k Business Loan in The Philippines - Essential Tips For Filipino Entrepreneurs To Follow

Improving your chances of securing a $100K business loan in the Philippines requires careful planning and strategic preparation. The best approach is to focus on your credit score, cash flow stability, business plan, and relationship with your bank, as this will enhance your loan application's effectiveness and increase the likelihood of its approval.

Here, take a look at the essential tips that will help you Filipino entrepreneurs acquire a $100k business loan in the Philippines without any hassle -

1. Strengthen Your Credit Score

Your credit score is one of the first things lenders assess, so to improve your chances, ensure your credit history is strong by paying bills on time, reducing outstanding debts, and avoiding unnecessary credit inquiries.

Also, regularly check your credit report for accuracy and address any issues that may negatively impact your score.

2. Prepare a Detailed Business Plan

A well-crafted business plan can significantly enhance your loan application by clearly outlining your business goals, financial projections, and how the loan will be used. Doing so will demonstrate a clear strategy and growth potential, which will make your application more compelling to lenders in the long term.

3. Demonstrate Stable Cash Flow

Lenders want to see that your business generates consistent revenue and has a healthy cash flow before they agree to a loan. To effectively display this, prepare detailed financial statements, including income statements, balance sheets, and cash flow projections, to show that your business can comfortably cover loan repayments, ultimately reassuring lenders of your creditworthiness.

4. Offer Collateral or a Personal Guarantee

Offering collateral or a personal guarantee can increase your chances of approval, especially for a large loan amount like $100K. This is mainly because collateral reduces the lender’s risk, as a personal guarantee shows your commitment to repaying the loan.

5. Build a Relationship with Your Bank

A strong relationship with your bank can be beneficial when applying for a loan, so it is a good idea to regularly engage with your bank manager, maintain open communication, and ensure your accounts are in good standing.

6. Consider Alternative Financing Options

If traditional loans are challenging to secure, explore alternative financing options like invoice financing, peer-to-peer lending, or government-backed loans. Depending on your business's specific situation, these options may have different eligibility criteria and could potentially be more accessible.

7. Keep Debt Levels Manageable

High levels of existing debt can be a red flag to lenders, so before you decide to apply for a $100K loan in the Philippines, first aim to reduce your current debt as much as possible. This is primarily because having a lower debt-to-income ratio will make your business more attractive to lenders and increase your chances of approval.

8. Provide Comprehensive Documentation

Ensure all required documentation is complete and accurate, including business registration, permits, financial statements, tax returns, and any other documents the lender requests.

Also Read: How Does A Bridge Loan Work For a Small Business?

Don’t wait for opportunities to pass by. Apply now for N90’s fast financing solutions and get the funds you need quickly. Unlock Quick Funding for Your Philippine SME Today!

Where To Apply For a $100k Business Loan in The Philippines - Best Options For Businesses To Consider

When applying for a $100K business loan in the Philippines, businesses have a variety of options to choose from, including commercial banks, government-backed loans, microfinance institutions, online lending platforms, and cooperative banks.

Each option has its own set of advantages and eligibility requirements, so Philippine businesses need to evaluate which lender best meets their financial needs and goals.

Here are some of the best options for Philippine businesses to consider to avail of a $100k business loan -

1. Commercial Banks

Commercial banks in the Philippines, such as BDO Unibank, Metrobank, and Bank of the Philippine Islands (BPI), are popular options for obtaining large business loans, as these banks offer a variety of loan products tailored to different business needs, including term loans, credit lines, and equipment financing.

2. Government-Backed Loans

Government agencies like the Department of Trade and Industry (DTI) and Small Business Corporation (SB Corp) offer loan programs specifically designed to support SMEs in the Philippines.

These government-backed loans often offer favorable terms, lower interest rates, and more extended repayment periods, making them ideal for businesses that may not meet the strict requirements of commercial banks.

3. Microfinance Institutions

Microfinance institutions like CARD SME Bank and ASA Philippines Foundation provide financial services to small businesses that may not qualify for traditional bank loans.

While MFIs typically offer smaller loan amounts, some institutions have loan products that can reach up to $100K for well-established businesses, as they often have more flexible eligibility criteria and faster approval processes.

4. Online Lending Platforms

Online lending platforms like First Circle and SeekCap have gained popularity for their convenience and speed because they offer a streamlined application process, often with quicker approval and disbursement times than traditional banks.

While their interest rates may be higher than those of other lenders, their ease of access and flexibility make them an attractive option for businesses, especially those needing fast funding.

5. Cooperative Banks

Cooperative banks, like MASS-SPECC Cooperative Development Center and Metro South Cooperative Bank, offer loans to their members, including small business owners. These institutions often provide more favorable loan terms and lower interest rates as they are focused on supporting their members' financial needs.

Also Read: Alternative Lending Options for Small Businesses

How To Effectively Use Your $100k Business Loan Funds - Key Practices For Philippine Businesses To Implement

Managing and utilizing a $100K business loan effectively requires careful planning, strategic investment, and ongoing monitoring. The best approach is to develop a detailed spending plan, focus on revenue-generating activities, and maintain strong cash flow.

By doing so, Philippine businesses can maximize the impact of their loan funds and set themselves up for long-term success. Here are some critical practices Filipino entrepreneurs can implement to manage and use their loan funds effectively -

1. Develop a Detailed Spending Plan

Before utilizing your loan funds, create a comprehensive spending plan that outlines how every peso will be allocated. You can do this by prioritizing the most critical areas of your business first, such as purchasing essential equipment, covering operational expenses, or investing in marketing.

This is important because having a detailed plan helps ensure that funds are used efficiently and aligned with your business objectives, thereby preventing overspending and maximizing the loan's impact.

2. Invest in Revenue-Generating Activities

Focus on using the loan to fund activities directly contributing to revenue generation. These could include expanding your product line, launching a marketing campaign, or entering new markets.

By prioritizing investments that have the potential to increase your income, you can boost your business’s financial health, as well as improve your ability to repay the loan on time.

3. Strengthen Your Cash Flow

Use part of the loan to bolster your cash flow and ensure you have access to ample liquidity to cover day-to-day operational expenses without financial strain.

This step is important because having a healthy cash flow allows you to manage unexpected costs, meet payroll, and maintain smooth operations even during slower business periods. Moreover, strengthening your cash flow reduces the risk of financial disruptions occurring and ensures your business remains stable for the long term.

4. Upgrade Equipment and Technology

Investing in new equipment or technology can significantly enhance your business’s efficiency and productivity, so it's a good idea to use the loan to upgrade outdated machinery, purchase new tools, or implement advanced software systems that streamline operations.

This is one of the best steps to take because improving your operational infrastructure can reduce costs, increase output, and keep you competitive in your industry.

5. Build an Emergency Fund

Allocate a portion of the loan to establish or grow an emergency fund, as this reserve can be used to address unforeseen challenges such as economic downturns, sudden market changes, or unexpected expenses.

Access to an emergency fund provides financial security and ensures your business can weather difficult times without compromising its operations.

6. Monitor Expenses and Adjust as Needed

Track loan funds regularly to ensure they are used according to your plan. One of the best ways to do this is by monitoring your expenses, as it allows you to identify areas where costs can be reduced or where additional investment may be needed.

7. Repay Debt Strategically

If part of the loan was intended to refinance existing debt, prioritize paying off high-interest loans first because by reducing your overall debt burden, you can free up more cash flow for other areas of your business and reduce the overall cost of borrowing.

In essence, strategic debt repayment helps improve your credit score and positions your business for better financing options in the future.

Also Read: Exploring Different Types of Business Finance

Choosing The Right Kind of Lender For a $100k Business Loan - Important Factors To Consider Before Selecting A Lender in The Philippines

Choosing the right lender for a $100K business loan in the Philippines requires carefully considering several factors, including interest rates, loan terms, eligibility criteria, and the lender’s reputation.

This is primarily because by thoroughly evaluating these aspects, you will be better able to select a lender that meets your financial needs and supports your business’s growth and stability.

Here are some of the essential factors to consider before selecting a lender to avail a $100k business loan in the Philippines -

1. Interest Rates and Fees

One of the first things to evaluate when choosing a lender is the interest rates and associated fees. You can do this by comparing different rates other lenders offer to determine which one provides the most competitive terms that suit your requirements.

Additionally, consider any hidden fees, such as origination fees, processing fees, or prepayment penalties, that could affect the overall cost of the loan, as receiving lower interest rates and incurring minimal fees will reduce your overall borrowing costs and make repayments more manageable.

2. Loan Terms and Repayment Flexibility

Ensure the loan term and repayment schedule align with your business’s cash flow and financial projections, as some lenders may offer short-term loans with higher monthly payments, while others may provide more extended repayment periods with lower monthly obligations.

Carefully assess your business’s ability to meet these payments without straining cash flow by always looking for lenders that offer flexible repayment options, such as the ability to make extra payments without penalties or adjust the payment schedule if needed.

3. Eligibility Criteria

Different lenders have varying eligibility requirements based on factors such as business size, industry, credit score, and operational history. So always ensure your business meets the lender’s criteria before applying to avoid wasting time and effort.

Additionally, if your company is new or has a lower credit score, consider lenders who specialize in working with startups or ones who offer more lenient credit requirements.

4. Collateral Requirements

Some lenders may require collateral to secure a $100K loan, while others offer unsecured loans that don’t need any assets as security. Therefore, evaluating whether your business can provide the necessary collateral and comprehend the potential risks involved before proceeding with the agreement is a good idea.

On the other hand, if you prefer not to pledge assets, seek out lenders who offer unsecured loans. However, it must be pointed out that these loans may come with higher interest rates due to the lender's increased risk.

5. Lender Reputation and Reliability

Businesses must consider the lender's reputation and reliability before proceeding with their applications, as availing a $100k business loan from a lender with a solid history of transparency, fair lending practices, and excellent customer service is more likely to provide a more positive borrowing experience.

You should research the lender’s track record, customer reviews, and industry reputation beforehand to determine if it is the right one for you.

6. Speed of Approval and Disbursement

If your business requires immediate funding, the speed of the loan approval and disbursement process is crucial, as some lenders, particularly online platforms, offer quicker processing times than traditional banks.

However, to ensure that speed does not come at the expense of higher costs or unfavorable terms, always balance your need for fast access to funds with the overall cost and conditions of the loan you may need to bear.

7. Customer Support and Communication

Effective communication and accessible customer support are essential throughout the loan process, so always choose a lender that offers responsive customer service and is willing to answer your questions and address concerns promptly.

This is an important point because a lender that provides clear communication and guidance can help you make your way through the complexities of the loan process more smoothly.

8. Additional Services and Resources

Some lenders offer additional services and resources that can benefit your business, such as financial planning tools, business advice, or access to networking opportunities.

Consider whether the lender provides value-added services that align with your business goals and can contribute to your long-term success. Sometimes, these extras make one lender appear more attractive than the other, even if their loan terms are similar.

Conclusion

Obtaining a $100K business loan can be a game-changer for your Philippine business, primarily because it provides your business with additional funds to achieve immense growth, enhance its operations, and overcome any financial challenges it might be facing or will face soon.

So, by carefully following the steps outlined in this detailed article on how to get a $100k business loan, from assessing your financial needs to choosing the right lender to prepare comprehensive documentation and effectively manage the loan, you will set your business up for success for the long term by receiving the funding that you need.

In essence, securing such a significant loan requires a business to make all the necessary preparations and conduct strategic financial planning. Always ensure that you and your business are in the correct position to utilize the various funding options available in the Philippines. This will enable you to give your business the financial push it needs to take it to the next level.

Frequently Asked Questions (FAQs)

1. How hard is it to get a $10,000 business loan?

Getting a $10,000 business loan can be easier than getting a more considerable amount because while these loans still require a business to possess a good credit score and have an overall stable financial health, smaller loan amounts pose less risk to lenders.

Consider exploring other options, such as online lenders, credit unions, or SBA microloans, to improve your chances of approval.

2. How to get a loan of $500,000?

Securing a $500,000 loan requires careful planning and preparation, so one of the best ways to start is by building a strong business plan, maintaining good credit, and showcasing solid financials. Explore options like SBA loans, traditional bank loans, or online lenders.

Additionally, it is also a good idea to compare the interest rates, terms, and fees being offered to you and your business to find the best fit for your business needs.

3. What factors might cause a bank to agree to lend money?

Several factors influence a bank's decision to lend money:

- Creditworthiness: A good credit score and history increase chances.

- Business viability: A solid business plan demonstrating potential profitability.

- Collateral: Offering assets as security can improve approval odds.

- Cash flow: Consistent and healthy cash flow is crucial.

- Repayment capacity: Demonstrating the ability to repay the loan on time.

- Economic conditions: Overall economic stability impacts lending decisions.

- Loan-to-value ratio: The loan amount should be reasonable compared to the asset's value.

4. What is the most prolonged business loan you can get?

The most prolonged business loan you can typically get is an SBA 504 or 7A loan, with terms of up to 25 years. These long-term loans are often used for significant investments like purchasing real estate, large equipment, or essential business expansion.

The extended repayment period allows for lower monthly payments, making it easier for businesses to manage cash flow while paying off the loan. However, the specific terms and length can vary depending on the lender, the type of loan, and the borrower’s financial profile.

Understanding the $100K Business Loan Application Process

1. Application process varies by lender

2. Higher qualifications due to loan size

3. Possible to qualify without perfect credit score or collateral

Types of $100K Business Loans

1. Small Business Term Loans: Lump sum, repaid with interest over a set period

2. Business Lines of Credit: Access capital as needed, pay interest on the amount drawn

3. Equipment Financing: Breakdown of asset costs over time, potential tax benefits

4. SBA Loans: Competitive rates, extended repayment terms, typically up to $5M

5. Revenue-Based Financing: Capital in exchange for a sales percentage, often with factor rates

Where to Apply for a $100K Business Loan

1. Traditional Banks: Stricter application process, lower interest rates

2. Online Lenders: More lenient with qualifications, quicker turnaround

How to Use Your $100K Business Loan Funds

1. Cover Expenses: Payroll, operation costs, free up cash flow

2. Purchase Inventory: Meeting demand, capitalizing on bulk discounts

3. Bridge Seasonal Gaps: Managing cash flow during off-seasons

4. Purchase New Equipment: Increasing efficiency, managing costs over time

5. Invest in Technology, Marketing, and Training: Improving processes, extending reach, enhancing team efficiency

Qualifying for a $100,000 Business Loan

1. Good Financial Standing: Showing profitability and stability

2. Collateral: Providing security for the loan

3. Credit Score Requirements: Personal and business credit scores, history of timely payments

4. Detailed Business Plan: Goals, income history, operational details

5. Financial & Legal Documents: Proof of identity, business licenses, detailed financial records

Improving Approval Chances for a $100K Business Loan

1. Strengthening credit score

2. Providing thorough and accurate documentation

3. Demonstrating a clear business plan and strategic growth potential

4. Ensuring sufficient collateral, if required

Choosing the Right Lender for a $100K Business Loan

1. Defining loan objectives and assessing specific loan use-cases

2. Comparing terms and interest rates offered by various lenders

3. Considering the reputation and support services of the lender

4. Matching the loan type to your specific business needs

Conclusion

1. Importance of choosing the right loan type and lender

2. Careful planning and preparation for the loan application

3. Utilizing the loan effectively to grow or maintain your business