Applying for and securing a loan in the Philippines can be challenging, especially when higher interest rates and limited loan amounts pose significant hurdles. Thankfully, a collateral loan, specifically using land as security, offers a viable solution for Filipino entrepreneurs to counter these issues.

In this blog, we'll examine the various types of land that can be used as collateral, understand the requirements involved, and learn about reputable institutions in the Philippines that offer such loans.

Additionally, we'll explore the potential benefits and possible risks of these loans to help Philippine businesses navigate through the loan process smoothly. Moreover, we will also take a closer look at the different nuances of collateral loans, explaining how using land can affect loan terms such as interest rates, loan amounts, and repayment periods.

What is a Collateral Loan, And Why Is It Important For Philippine Businesses?

A collateral loan, also known as a secured loan, is a type of loan in which the borrower pledges an asset to secure the loan. The asset, often referred to as collateral, acts as a safety net for the lender.

However, it must be noted that the lender can seize the collateral if the borrower defaults on the loan to recover the loss. Typical forms of collateral include property, vehicles, equipment, or other valuable items.

Here, take a look at some of the vital importance of collateral loans for Philippine businesses -

1. Impact on Interest Rates

One of the main advantages of collateral loans is the lower interest rate. Unsecured loans often come with high interest rates because the lender is taking on more risk without a guarantee of repayment beyond the borrower's creditworthiness. In contrast, collateral loans provide security for the lender, allowing them to offer lower interest rates.

2. Loan Amount Received

It is common for lenders to provide a loan amount that is 70% to 80% of the property's value. You can benefit from this higher loanable amount if you need a more significant sum of money.

3. Generous Repayment Tenure

These can extend up to 48 months, giving you ample time to repay the loan without undue financial strain. Extended repayment periods make monthly installments more manageable and the loan process less stressful.

Also Read: Getting a Fast Loan in 15 Minutes in the Philippines

Types of Land Used as Collateral

Various types of land can be used as collateral when securing a loan in the Philippines, each offering unique advantages and subject to different considerations.

Here's a closer look at the different types of land that can be used as collateral when applying for a collateral loan in the Philippines -

1. Residential Properties

This category includes houses and lots, condominium units, and residential lots, and lenders mostly find these types of properties attractive due to their stable and valuable nature. Financial institutions such as AsiaLink Finance often extend loans with residential properties as security.

2. Commercial Properties

Commercial properties, including buildings and lots used for various business operations, can be solid collateral, especially for business-related loans. Business owners can use these properties to secure loans to expand operations, purchase additional assets, or manage cash flow.

3. Agricultural Lands

Agricultural land, used for farming and other agricultural activities, is another interesting type of collateral. Using agricultural land as collateral can be intricate due to specific regulations and restrictions, particularly concerning foreign ownership.

Under the 1987 Philippine Constitution, stringent rules govern using agricultural land as collateral. The government allows private corporations to lease public agricultural land up to 1000 hectares, while Filipino citizens can lease up to 500 hectares or acquire up to 12 hectares via purchase, homestead, or grant.

The government designed these regulatory frameworks to manage agricultural land carefully, preserving its primary purpose and preventing misuse.

Despite these restrictions, agricultural land remains a viable collateral option for those in the farming sector, as it provides a means to secure funding for expanding operations, purchasing farming equipment, or other developmental projects.

Also Read: Pros and Cons of Debt Consolidation in the Philippines

Requirements for Using Land as Collateral - Important Points For Philippine Businesses To Remember

When considering using land as collateral for a loan in the Philippines, it's essential to prepare specific documents and meet certain requirements to ensure a smooth and successful transaction.

Here's what you'll ideally need to present to secure a loan using land as collateral -

1. Original Land Title

The original land title is the cornerstone of using land as collateral. This document serves as the primary proof of property ownership, so it is vital always to ensure that the title is clear of any liens, encumbrances, or restrictions. Lenders will carefully analyze the title to confirm that the land can secure the loan without running into any legal complications.

2. Proof of Income

Providing proof of income is mandatory to demonstrate your ability to repay the loan. This could include pay slips, employment certificates, bank statements, or tax returns. This is because lenders need to see a reliable and consistent source of income to ensure that they are not taking on excessive risk by granting the loan.

3. Tax Declaration

An updated tax declaration is another essential requirement, as this document proves that you are up-to-date with your property taxes. It also serves as an additional verification of the property’s status and ensures that there are no outstanding tax liabilities that could complicate the loan process.

4. Recent Property Photo

Include a recent photograph of the property. This allows lenders to assess the current condition and approximate the market value of the land. Ensure the photo is clear and provides a comprehensive view of the property.

Also Read: Understanding and Solving Common Cash Flow Problems

N90’s fast financing solutions are designed for your success. Apply today and receive loan approvals within 24 hours! Get the funding your Philippine SME needs quickly!

How To Get a Loan Using Land as Collateral - A Step-By-Step Application Process Guide For Businesses

Securing a loan using land as collateral is a common and effective way for businesses to access significant funding. Here’s a step-by-step guide to help you navigate the application process efficiently -

1. Assess the Value of Your Land

Begin by evaluating the market value of the land you intend to use as collateral. This can be done through a professional appraiser or by researching comparable land values in the area. Knowing the value will help you determine how much you can borrow and what terms you might expect from lenders.

2. Gather Necessary Documents

Prepare all required documents related to the land and your business.

Key documents include the following -

- Land Title (Transfer Certificate of Title or TCT)

- Tax Declaration and Receipts

- Survey Plan and Lot Plan

- Business Registration Certificates

- Financial Statements (Income Statement, Balance Sheet, Cash Flow Statement)

- Tax Identification Number (TIN) and business tax returns

3. Choose the Right Lender

Research various banks and financial institutions that offer land-secured loans and compare their interest rates, loan terms, fees, and customer service. Some lenders may have specific requirements or provide better terms for certain types of land or businesses, so choosing a lender that aligns perfectly with your needs is essential.

4. Submit a Loan Application

Once you’ve selected a lender, submit a formal loan application. This application will typically require you to provide detailed information about your business, the land being used as collateral, and the amount you wish to borrow. Ensure that your application is complete and accurate to avoid delays in processing.

5. Undergo Land Appraisal and Verification

The lender will likely conduct their own appraisal of the land to verify its value, and they may also check for any legal issues related to the property. This step is crucial, as the appraised value will determine the loan amount you can secure, so be prepared for the lender’s representatives to visit the property for inspection.

6. Review the Loan Offer

After the appraisal, the lender will present you with a loan offer. Review the terms carefully, including the interest rate, repayment schedule, and any associated fees. Ensure that the terms are favorable and manageable for your business’s financial situation, and if necessary, negotiate with the lender to get better terms.

7. Sign the Loan Agreement

You will sign the loan agreement once you agree to the loan terms. This legally binding document outlines your obligations, including repayment terms and conditions. Ensure you understand all the agreement's aspects before signing, and consult with a legal advisor if needed.

8. Register the Mortgage

The lender will require the land to be mortgaged, which involves registering the mortgage with the Registry of Deeds. This process legally records the lender’s interest in the property, and the land title will indicate that the property is mortgaged until the loan is fully repaid.

9. Receive the Loan Proceeds

After the mortgage is registered, the lender will disburse the loan proceeds to your business bank account. Depending on the lender, this process could take several days to a few weeks.

Using land as collateral is a standard method individuals use to finance their businesses. Read this Reddit thread to hear what other Filipino entrepreneurs have to say about this.

Also Read: What is a Business Loan, and How Does it Work?

Where to Get Loans Using Land as Collateral in the Philippines - Best Avenues For Businesses To Consider

If you are considering using your land as collateral for a loan in the Philippines, several financial institutions offer such services.

Here are some of the most prominent options available -

1. AsiaLink Finance

AsiaLink Finance offers a Real Estate Mortgage loan, which allows borrowers to use the value of their property as collateral. It caters to various properties, including residential lots, condominiums, and commercial establishments.

However, AsiaLink Finance does not accept agricultural lots as collateral. This option suits those needing substantial financing, with a maximum loan approval of up to PHP 15 million per client.

2. Security Bank

Security Bank, one of the largest banks in the country, offers a Home Equity Loan that allows borrowers to leverage the value of their property. This loan is versatile and can be used for various needs, such as home renovations, business capital, education, or personal use.

3. Maybank

Maybank, another significant banking institution in Southeast Asia with operations in the Philippines, also offers a Home Equity Loan. Like Security Bank, Maybank's loan allows you to use your property as collateral.

Loan proceeds can be allocated for various purposes, including home improvement projects, funding a business venture, supporting educational endeavours, or meeting other personal financial needs.

4. Nala Collateral Loan

Nala provides a Land Title Collateral Loan, which is designed with the borrower’s financial capacity in mind. Their loan terms strive to be both reasonable and equitable.

Nala’s Land Title Collateral Loan can be utilized for various purposes such as financing house construction, home renovation, business capital, covering medical expenses, or educational and personal needs. This lending institution ensures that loan terms are tailored to the borrowers' financial capabilities, making it a borrower-friendly option.

5. GDFI Car Collateral Loan

GDFI Car Collateral Loan is a financial product Global Dominion Financing Incorporated (GDFI) offers in the Philippines. It is designed to give individuals quick cash access by using their car as collateral.

This loan allows car owners to utilize the value of their vehicle to obtain a substantial loan amount, typically with lower interest rates than unsecured loans. The GDFI Car Collateral Loan is ideal for those needing immediate funds for personal or business needs, offering flexible repayment terms while allowing borrowers to retain and use their vehicle during the loan period.

6. Blend PH Auto-Sangla Loan

Blend PH Auto-Sangla Loan is a financial product offered by Blend PH, a peer-to-peer lending platform in the Philippines. This loan allows vehicle owners to use their car as collateral to secure a loan quickly and easily.

The term ‘Auto-Sangla’ refers to the process of pawning a car, providing borrowers with access to funds without selling their vehicle. Blend PH offers competitive interest rates and flexible repayment terms, making it an attractive option for those needing immediate cash for personal or business purposes while retaining the use of their vehicle.

7. JCT EZ Land Title Collateral Loan

The JCT EZ Land Title Collateral Loan is a financial product offered by JCT EZ Loan, designed to provide individuals and businesses with easy access to funds by using land titles as collateral. This loan is ideal for those who own real estate but need quick liquidity for various purposes, such as business expansion, debt consolidation, or personal expenses.

With flexible terms, competitive interest rates, and a straightforward application process, the JCT EZ Land Title Collateral Loan offers a practical solution for borrowers seeking substantial financing without selling their property. This loan helps unlock the value of your land while retaining ownership.

Also Read: Finding Low-Interest Business Loans in the Philippines

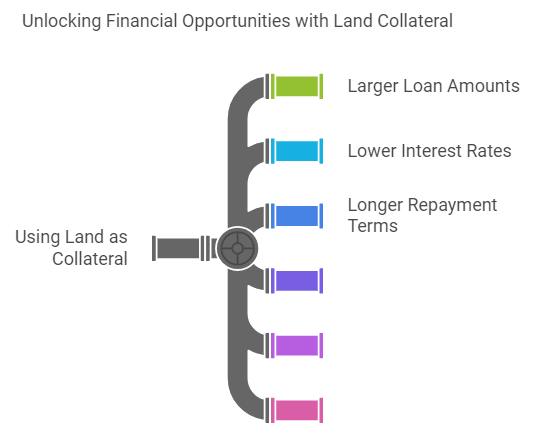

Benefits of Using Land as Collateral

Using land as collateral can provide several advantages for individuals and businesses seeking to secure loans or financing.

Here are some key benefits of doing so -

1. Larger Loan Amounts

Land is considered a valuable asset, often enabling borrowers to secure more significant loan amounts than unsecured loans. This makes it ideal for funding significant investments or large-scale projects.

2. Lower Interest Rates

Loans secured with land typically have lower interest rates because the collateral reduces the lender's risk. This can result in significant savings for businesses over the life of the loan.

3. Longer Repayment Terms

Lenders are more likely to offer extended repayment terms when land is used as collateral. Longer terms mean lower monthly payments, making cash flow easier to manage.

4. Easier Loan Approval

Using land as collateral can increase the chances of loan approval, even for borrowers with less-than-perfect credit. The collateral assures the lender, making them more willing to approve the loan.

5. Flexibility in Loan Usage

Loans secured with land are often flexible regarding how the funds can be used. Borrowers can use the loan for various purposes, including business expansion, home construction, or debt consolidation.

6. Potential for Larger Capital Access

Using land as collateral can also allow businesses to access more significant amounts of capital, which can be crucial for expansion, purchasing new equipment, or taking advantage of growth opportunities.

7. Improved Negotiation Power

Having land as collateral gives borrowers greater leverage in negotiating loan terms, such as interest rates, repayment schedules, and other conditions that could be more favorable.

8. Asset Retention

Unlike selling land to raise funds, using land as collateral allows the borrower to retain ownership of the asset. The land remains the borrower's property as long as the loan they repay the loan.

Also Read: Non-Collateral Startup Business Loans in the Philippines

Potential Risks of Using Land as Collateral

Using land as collateral to secure a loan in the Philippines might seem appealing, but it comes with significant risks that borrowers must consider.

Here, take a look at the potential risks Philippine businesses must be aware of when using their land as collateral to secure a loan -

1. Risk of Losing the Property

One of the most significant risks is losing your property if you can’t meet the loan repayment terms. If you default, the lender can legally seize and sell your land to cover their losses. This could have severe financial and personal impacts, especially if the land has sentimental or substantial economic value.

2. Potential Complications in Property Transfer

Issues can also arise if the land title or ownership isn’t clear. Problems like liens, encumbrances, easements, or land-use restrictions can delay the loan approval process and complicate your financial plans. It’s essential to resolve these issues before using land as collateral.

3. Valuation Challenges for Certain Types of Land

Valuing land can be tricky because natural disasters, environmental hazards, and market fluctuations can all affect the property’s value, making it hard for lenders to appraise it. This could result in lower loan amounts and higher interest rates to cushion potential defaults.

4. Legal and Financial Implications

Using land as collateral has its own legal and financial challenges. Besides, the risk of losing your property can also impact your debt-to-income ratio, mainly if the land is already mortgaged.

Be prepared to bear additional fees like processing, notarial, and late payment charges. Lenders usually conduct thorough checks and market analyses to evaluate the land’s value and risks, often resulting in strict loan terms.

5. Negative Environmental and Community Impacts

Using land as collateral can have broader implications beyond personal risk. Using the land for projects that don’t follow sustainable practices or local regulations could harm the environment and local communities. This can degrade natural landscapes and displace residents.

Do you still need to decide whether to use your land as collateral when applying for a loan in the Philippines? Check out this video. It highlights the hidden risks and legal considerations when using land as collateral.

Conclusion

When considering a loan using land as collateral in the Philippines, the benefits are compelling because utilizing land for a loan typically offers more favorable interest rates and higher loan amounts than unsecured loans.

Using land as collateral can provide access to significant capital, which may be used for various purposes, such as expanding a business, renovating a home, or covering emergency expenses. The stability and value of land act as a solid guarantee for lenders, which can simplify the overall loan approval process and terms offered.

However, it is also crucial to recognize the inherent risks of availing a loan using your land as collateral. The most significant risk is the potential loss of your land if you default on the loan. This could have long-term repercussions, including losing a family asset or a critical piece of property that might be appreciated over time.

Furthermore, using land as collateral can involve intricate legal and administrative processes, and mishandling these could lead to legal disputes or future complications for you and your business. So, it is of utmost importance that Philippine companies be completely aware of all the processes before applying for a loan using their land as collateral.

Frequently Asked Questions (FAQs)

1. What is the most prominent VC in the Philippines?

Kickstart Ventures is considered one of the Philippines' most significant venture capital (VC) firms. It is a subsidiary of Globe Telecom and manages a substantial fund that invests locally and globally in tech startups. Kickstart Ventures focuses on early- to growth-stage companies, providing capital, strategic support, and access to a broad network.

2. What is the best investment company in the Philippines?

Some of the well-regarded investment firms are as follows -

- BPI Investment Management: Offers a wide range of investment products and services.

- Metrobank Investment Banking: Provides investment banking and wealth management services.

- Sun Life Investment Management: Specializes in mutual funds and retirement planning.

3. What is a venture capitalist in the Philippines?

In the Philippines, a venture capitalist is an individual or firm that invests in early-stage companies. They provide capital in exchange for equity ownership and generate a substantial return on their investment when the company exits.

Venture capitalists often offer mentorship, guidance, and industry expertise to help the companies they invest in succeed.

4. Who owns most of the businesses in the Philippines?

In the Philippines, a significant portion of businesses are owned by Filipino families. These family-owned businesses often span generations and encompass various industries, from retail and manufacturing to real estate and finance.

While there are also foreign-owned and publicly traded companies, family-owned businesses remain dominant in the Philippine economy.