Starting a money lending business in the Philippines can be a profitable venture, given the demand for quick access to funds. Many Filipinos, especially those without access to traditional banking, rely on money lenders for personal and business loans.

However, this business requires a thorough understanding of legal requirements, risk management, and effective lending practices.

Therefore, to help aspiring Filipino professionals start off on the right foot, this blog will provide an in-depth overview of the money-lending industry in the Philippines and examine all the elements required to start a long-term money-lending business.

The components include legal requirements, various lending models, business plan development, and more. Moreover, you'll also explore how to secure funding and establish operations, making a firm foundational understanding crucial for success in this venture. So, without any more delays, let us get down to it.

Money Lending Businesses in The Philippines - A Brief Overview

Money lending businesses in the Philippines are financial entities or individuals that provide loans to borrowers, often outside the traditional banking system. These businesses offer personal, business, or emergency loans to individuals or small enterprises who may not have access to formal banking services.

They operate under various models, such as microfinance institutions, pawnshops, private lenders, or online lending platforms, and typically charge interest on the loans they provide and may require collateral or guarantors, depending on the amount and type of loan.

Moreover, they are regulated by the Securities and Exchange Commission (SEC) and must comply with the Lending Company Regulation Act (RA 9474) to ensure fair and legal lending practices.

The primary income source for money lending businesses comes from the interest rates charged on the borrowed principal amount. These rates are generally higher than those offered by conventional banks, usually ranging between 15% and 20% for private money lending.

Essentially, these businesses fill a critical gap in financial access, especially for low-income individuals and small businesses.

Furthermore, compliance with other legal requirements, such as usury laws that limit interest rates, is essential. These laws protect borrowers from excessive interest charges while ensuring lending businesses operate within legal limits.

Also Read: 6 Things You Need for Small Business Loan Requirements

What is the Importance of Money Lending Businesses To The Philippine Economy?

Money lending businesses are crucial in providing accessible financial services to Filipinos, especially in underserved communities. They fill the gap left by traditional banks, helping individuals and small businesses meet their financial needs.

Here’s why they are essential for individuals and businesses alike in the Philippines -

1. Financial Inclusion

Money lending businesses help promote financial inclusion by offering loans to individuals and small businesses that do not qualify for bank loans, particularly those in rural areas. This allows more Filipinos to access credit and grow their financial capabilities.

2. Support for Small and Medium Enterprises (SMEs)

Many small businesses rely on money lenders for capital to start or expand their operations. By offering flexible loan options, money lending businesses help drive the growth of SMEs, which are vital contributors to the Philippine economy.

3. Job Creation

The money lending industry generates employment opportunities, from loan officers to administrative staff. Additionally, providing capital to businesses indirectly contributes to job creation in various sectors.

4. Economic Growth

Money-lending businesses stimulate economic activity by injecting much-needed capital into local economies. Credit availability allows individuals and companies to purchase goods, invest in new ventures, and generate income.

5. Emergency Financial Assistance

Money lenders provide quick access to funds for Filipinos facing financial emergencies, such as medical expenses, education fees, or unexpected household repairs, which supports the overall economic stability of families and communities.

Also Read: Best Short-Term Business Loans for Fast Financing

Legal and Regulatory Nuances Involved in Starting a Money Lending Business in The Philippines

Starting a money lending business in the Philippines involves navigating several legal and regulatory requirements. These rules are designed to ensure fair lending practices, protect borrowers, and regulate the industry’s growth in line with the country’s financial policies.

Here are the critical legal and regulatory considerations to keep in mind when starting a money-lending business in the Philippines -

1. Registration with the SEC

Money lending businesses must register with the Securities and Exchange Commission (SEC) under the Lending Company Regulation Act (RA 9474).

The SEC grants licenses and monitors lending practices to ensure compliance with legal requirements. Operating without this registration is illegal and subject to penalties.

2. Minimum Paid-Up Capital

According to RA 9474, lending companies must have a minimum paid-up capital of PHP 1 million. This capital requirement ensures the business has sufficient funds to operate and can cover loan defaults if necessary.

3. Interest Rate Regulations

Interest rates for money lending businesses must comply with Philippine laws. The BSP (Bangko Sentral ng Pilipinas) has set guidelines to ensure that interest rates are fair, with recent regulations setting a 6% monthly cap on interest rates for loans offered by lending and financing companies.

4. Loan Agreement Requirements

Lending companies must provide borrowers with written loan agreements detailing the loan amount, interest rate, payment terms, and any fees. These agreements must be clear and transparent to avoid disputes and ensure borrowers fully understand the terms of their loans.

5. Consumer Protection Laws

To avoid predatory lending practices, money lending businesses must comply with consumer protection regulations. These laws include disclosing all fees, avoiding deceptive advertising, and offering fair loan terms.

Non-compliance with these protections can result in penalties or loss of licensing.

6. Compliance with Anti-Money Laundering (AML) Laws

Lending businesses must also comply with the Anti-Money Laundering Act (AMLA), which includes implementing customer due diligence and reporting suspicious transactions to the Anti-Money Laundering Council (AMLC). This prevents illegal financial activities through the lending system.

7. Taxation

Money lending businesses are subject to taxation, including corporate taxes, business permits, and other local taxes. Ensuring compliance with the Bureau of Internal Revenue (BIR) is essential to avoid legal issues and penalties.

Are you considering starting your own money-lending business without compiling with legal regulations? Read this Reddit thread before you proceed. It discusses why legal and regulatory compliance is crucial for a new business to operate smoothly in the lending industry.

Also Read: Common Types of Bank Loans in the Philippines

Types of Lending Models Offered in The Philippines

The lending industry in the Philippines offers various models to cater to different borrower needs. Each model serves a specific purpose, whether for individuals, small businesses, or larger enterprises.

Here are the primary lending models offered by lending institutions in the Philippines to individuals and businesses alike -

1. Traditional Bank Lending

Banks in the Philippines, such as BDO, BPI, and Metrobank, offer personal, business, or corporate loans. They usually require extensive documentation, including credit checks, and have more stringent eligibility criteria.

Traditional bank lending is favored for its lower interest rates and structured repayment plans, but processing can take longer than other models.

2. Microfinance Lending

Microfinance institutions, like CARD Bank and ASA Philippines, provide small loans to individuals or micro-businesses, especially in rural areas. This model is designed to support low-income individuals or those with limited access to traditional banking.

It’s popular for short-term loans with smaller amounts, often without the need for collateral.

3. Peer-to-Peer (P2P) Lending

P2P platforms like LendPinoy and Acudeen allow individuals to lend directly to borrowers through online platforms. This lending model cuts out traditional financial institutions, offering faster approval processes and more flexibility for both lenders and borrowers.

4. Pawnshop Lending

Pawnshops, such as Cebuana Lhuillier and M Lhuillier, provide collateral-based lending by offering loans in exchange for valuable items like jewelry, electronics, or property.

These loans are quick and easy to access but typically have higher interest rates and shorter repayment periods. Borrowers must repay within a set time or risk losing their collateral.

5. Online Lending Platforms

Digital lending companies, including Cashalo, Tala, and UnaCash, provide quick, short-term loans through mobile apps. These platforms use less stringent requirements, allowing fast approval with minimal documentation.

They cater to those needing emergency funds or those without traditional credit histories but often come with higher interest rates.

6. Cooperative Lending

Cooperatives, like the Philippine Cooperative Central Fund Federation (PCF), offer loans to their members, often at lower interest rates than banks. These cooperatives pool resources from members and use the funds to provide financial assistance.

This model benefits members of specific communities or industries who prefer a more collaborative financing approach.

Also Read: Applying for a Small Business Loan: 5 Steps to Get Approved

Get the financial support your Philippine SME needs with N90’s Fast Financing Solutions. Apply today and get potential loan approvals within 24 hours! Give your business the financial boost it needs to excel without any hassle!

How To Create a Comprehensive Business Plan To Start a Money Lending Business in The Philippines

Establishing a successful money lending business starts with a comprehensive business plan. Starting a money lending business in the Philippines requires a clear and detailed business plan that covers legal, financial, and operational strategies.

This plan is crucial because it ensures regulatory compliance, attracts investors, and manages risks effectively. Here’s how to create a comprehensive business plan before starting a money-lending business in the Philippines -

1. Executive Summary

This section provides an overview of your business, outlining the purpose of your money-lending business and the market opportunity. Include your business’s mission, objectives, and a brief description of the services you will offer.

2. Business Structure and Legal Requirements

Define the legal structure of your business (e.g., sole proprietorship, corporation). Include details on registering with the Securities and Exchange Commission (SEC) under the Lending Company Regulation Act (RA 9474) and securing all necessary permits, including a certificate of authority.

Research all SEC and Bureau of Internal Revenue (BIR) requirements for lending companies in the Philippines.

3. Market Research and Analysis

Research to understand the market demand for lending services in your target areas. Analyze the competition, identify your target demographic, and assess the economic conditions that could impact your business.

4. Loan Products and Services

Outline the types of loans you will offer (e.g., personal, business, microloans) and detail the terms, including loan amounts, interest rates, and repayment periods. Include specific lending models, such as peer-to-peer lending or microfinance.

5. Financial Plan

Develop a financial plan that includes your initial investment, startup costs, and projected revenue. List your funding sources, such as personal savings, investors, or loans, and include a break-even analysis, cash flow projections, and financial forecasting for the next 3-5 years.

6. Marketing and Sales Strategy

Develop a marketing plan to promote your services. This could include social media marketing, partnerships with local businesses, or offering referral bonuses. Define your unique selling proposition (USP) that differentiates your lending business from competitors.

7. Risk Management and Contingency Plan

Includes a risk management strategy to handle loan defaults and economic downturns. Identify potential risks (e.g., high default rates) and how you will mitigate them (e.g., requiring collateral or guarantors).

8. Operations Plan

Detail the day-to-day operations of your money lending business, including loan processing, customer service, and collections. Outline the technologies or software you will use to track loans and payments.

Include a timeline for setting up operations, hiring staff, and launching your services.

9. Compliance with Anti-Money Laundering (AML) Laws

Your business must comply with the Anti-Money Laundering Act (AMLA). Include processes for customer due diligence and reporting suspicious transactions to the Anti-Money Laundering Council (AMLC).

Outline steps for training staff on AML compliance and customer screening.

10. Exit Strategy

Outline your exit strategy if you decide to close the business or sell it. Include plans for transferring operations, liquidating assets, or merging with other financial institutions.

Also Read: Benefits and Disadvantages of Small Business Loans

How To Secure Funding and Capital To Start a Money Lending Business in The Philippines

Starting a money lending business in the Philippines requires adequate funding to meet legal capital requirements and operate effectively. Securing the right amount of capital is essential for sustainability and growth.

Here, take a look at the ways to secure funding to start a money-lending business in the Philippines -

1. Personal Savings

Using personal savings is one of the most straightforward ways to fund your money-lending business. It allows you to retain complete company control without taking on debt or diluting ownership.

Calculate the minimum capital required, at least PHP 1 million, and assess how much you can fund through your savings.

2. Bank Loans

Applying for a business loan from a bank is a standard method of securing startup capital. Philippine banks like BPI, BDO, and Metrobank offer various loan products for small and medium enterprises (SMEs).

Prepare a solid business plan and financial projections to improve your chances of securing a loan. Ensure compliance with the bank's collateral and credit score requirements.

3. Government Funding Programs

The Department of Trade and Industry (DTI) and other government agencies offer funding programs to support small businesses. Programs like Pondo sa Pagbabago at Pag-asenso (P3) provide low-interest loans to micro-enterprises.

Explore DTI and Small Business Corporation (SB Corp) funding programs and see if your business qualifies for financial assistance.

4. Private Investors

You can seek funding from private investors or venture capitalists who may be interested in financing your money lending business in exchange for equity or profit-sharing.

Pitch your business plan to investors, showcasing potential profitability and growth opportunities. Highlight the demand for lending services in underserved markets.

5. Cooperative Lending or Peer-to-Peer Lending

Some cooperative lending models or peer-to-peer (P2P) lending platforms can provide startup capital by connecting you with individuals willing to invest in your business.

Join a cooperative or use P2P lending platforms like LendPinoy or Acudeen to raise funds from private lenders.

6. Microfinance Institutions

Microfinance institutions offer small loans with low interest rates, making them suitable for securing initial capital. These institutions are geared toward supporting small businesses and entrepreneurs.

Approach microfinance institutions like CARD Bank or ASA Philippines to inquire about loan options for your startup.

7. Angel Investors

Angel investors are individuals who invest in startups in exchange for ownership equity or convertible debt. They may provide capital, mentorship, and networking opportunities.

Action: Network with potential angel investors through business events or online platforms and present your business plan. Be prepared to negotiate terms that align with your business goals.

8. Crowdfunding

Crowdfunding platforms can be used to raise capital by collecting small contributions from a large group of people. While this method is more common for product-based businesses, it can be adapted for a lending business with a vital community aspect.

Set up a campaign on crowdfunding platforms like Kickstarter or GoGetFunding. Clearly explain your business’s mission and how contributors can benefit.

Are you still unsure how to start a money-lending business? Check out this video. It explains how the average person can start a private money lending business. It also provides practical steps to maintain a successful venture and a few prominent challenges they might have to overcome.

Also Read: Differences and Types of Commercial and Business Loans

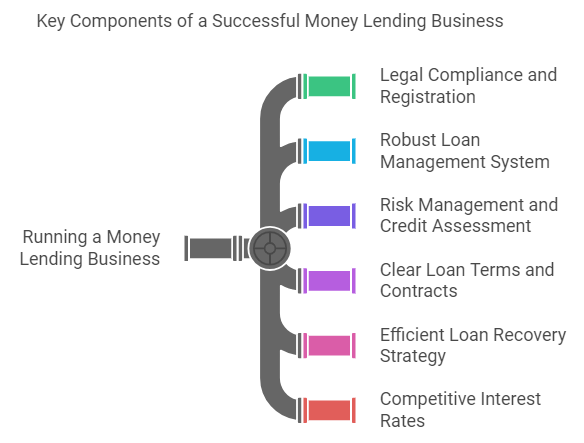

Components Required To Ensure a Philippine Money Lending Business Runs Smoothly

Several critical components must be in place to ensure that a money lending business in the Philippines operates efficiently and complies with regulations. These elements are crucial for the business’s sustainability, customer satisfaction, and legal compliance.

Here are the critical components required to run a money lending business effectively in the Philippines -

1. Legal Compliance and Registration

All money-lending businesses in the Philippines must register with the Securities and Exchange Commission (SEC) under the Lending Company Regulation Act (RA 9474). Proper licenses and permits ensure that the business operates legally and avoids penalties.

Complete all necessary registrations with the SEC, Bureau of Internal Revenue (BIR), and local government units (LGUs).

2. Robust Loan Management System

Implement a reliable loan management system (LMS) to track loan applications, disbursements, repayments, and defaults. This software automates processes, ensures accuracy, and helps manage multiple accounts efficiently.

Cloud-based platforms can provide real-time monitoring of loan portfolios and generate reports for better decision-making.

3. Risk Management and Credit Assessment

Proper risk management ensures that the business minimizes defaults. Thorough credit assessments of potential borrowers are essential to determining their ability to repay loans.

Implement strict credit checks and establish clear policies for collateral or guarantors to mitigate risks.

4. Clear Loan Terms and Contracts

Transparency in loan agreements is critical to building trust with borrowers. Loan terms, including interest rates, repayment schedules, and penalties for late payments, should be clearly outlined in written contracts.

Ensure contracts comply with the Truth in Lending Act (RA 3765) and are easy for borrowers to understand.

5. Efficient Loan Recovery Strategy

Implementing a loan recovery strategy is crucial to avoid financial losses. Develop a collection process that includes follow-up reminders and legal actions when necessary.

Employ collection agents and use automated reminders for late payments to ensure compliance with the Fair Debt Collection Practices Act (RA 6552).

6. Competitive Interest Rates

Offering competitive yet sustainable interest rates is essential to attract borrowers while ensuring profitability. Interest rates should be aligned with Bangko Sentral ng Pilipinas (BSP) guidelines, which set a monthly cap of 6%.

Regularly review market trends and adjust interest rates to remain competitive while complying with regulations.

7. Customer Service and Relationship Management

Building a solid relationship with clients ensures long-term success. Providing excellent customer service, quick loan approvals, and transparent communication fosters trust and client retention.

Train staff in customer relationship management (CRM) and ensure prompt, professional responses to inquiries.

8. Capital and Financial Planning

Adequate capital reserves are essential for handling loan disbursements and absorbing potential default losses. A well-structured financial plan helps maintain liquidity and achieve growth targets.

Secure enough initial capital and maintain an emergency fund to cover operational costs and loan defaults.

9. Marketing and Outreach Strategies

Effective marketing is vital to reaching potential borrowers. Digital marketing strategies, including social media, can help attract more clients, especially in underserved areas.

Develop a marketing plan highlighting your business's unique selling points, such as faster approval times or lower interest rates.

Also Read: Non-Collateral Startup Business Loans in the Philippines

Marketing and Growth Strategies To Implement To Grow Your Money Lending Business in The Philippines

Effective marketing and growth strategies are crucial in expanding your money-lending business. With the rapid shift to digital, online marketing has become indispensable.

Here's how you can harness marketing and proven growth strategies to start and grow your money-lending business in the Philippines -

1. Utilize Digital Marketing

Digital marketing is a cost-effective way to reach a wider audience. Promote your lending services on social media platforms like Facebook and Instagram, which are highly popular in the Philippines.

Run targeted ads, create engaging content, and offer promotions to attract potential borrowers. Use SEO strategies to improve your website's visibility on search engines.

2. Develop Referral Programs

Referral programs encourage satisfied customers to bring in new clients by offering incentives such as reduced interest rates or cashback rewards. This can boost your business through word-of-mouth marketing.

Create an easy-to-understand referral program with clear incentives for both the referrer and the new client. Promote the program through email campaigns and social media.

3. Offer Flexible Loan Products

Tailor loan products to suit the diverse needs of borrowers, such as microloans, small business loans, and personal loans with varying repayment terms. This ensures you cater to different market segments.

Assess customer needs and create loan packages that include flexible payment options, interest rates, and loan amounts to attract a broader range of clients.

4. Focus on Customer Service Excellence

Providing exceptional customer service builds trust and loyalty. Quick loan approvals, transparent terms, and responsive customer support are essential for customer satisfaction.

Train staff to provide professional, prompt, and helpful assistance. CRM systems track client interactions and ensure personalized service.

5. Collaborate with Local Businesses

Form partnerships with local businesses and cooperatives to expand your lending services. This will help you reach customers who are already part of a trusted community.

Develop loan programs specifically catering to small businesses or cooperatives in underserved areas. Collaborate with local organizations to promote these products.

6. Implement Financial Literacy Programs

Educating your target market on financial management and responsible borrowing can increase their trust and confidence in your services. Financially literate clients are more likely to make timely repayments.

Organize financial literacy workshops or offer free online resources and webinars. This also positions your business as a trusted financial advisor, further strengthening your client relationship.

7. Utilize Mobile Lending Apps

Mobile lending platforms are becoming increasingly popular in the Philippines. Offering a mobile app can make it more convenient for clients to apply for loans, check balances, and make payments.

Develop a user-friendly mobile app that allows borrowers to easily apply for loans and manage their accounts. Ensure secure payment gateways and timely notifications to encourage customer engagement.

8. Diversify Lending Channels

In addition to traditional lending, explore peer-to-peer (P2P) lending, crowdfunding, or partnerships with fintech companies. Diversifying lending channels can increase your market reach and attract tech-savvy borrowers.

Research potential partnerships with fintech platforms or develop your own P2P lending system to expand your business.

Conclusion

To conclude, as we have seen from this article, the potential for profitability in the money lending business is substantial, yet it hinges on careful planning and strict compliance with legal standards.

To thrive, aspiring Filipino entrepreneurs must develop a deep understanding of market demand and the legal landscape governing money lending. A lender can make the right lending decisions that meet current market needs by staying informed about borrower profiles and economic signals.

Moreover, flexibility in business strategies is imperative. As economic conditions fluctuate, so do borrowing needs and risks. Adapting to these changes ensures that a lender can manage risk effectively while maintaining a steady stream of clients.

Balancing interest rates to optimize profitability without significantly increasing default rates is a delicate task that requires constant vigilance and adjustment based on market conditions.

In summary, the ability to pivot strategies, stay compliant, and understand the market deeply determines the success of a money lending venture. With the right approach, the opportunities in this field are plentiful.

Frequently Asked Questions (FAQs)

1. Are lending businesses profitable in the Philippines?

Yes, lending businesses can be profitable in the Philippines due to the high demand for personal, business, and microloans. With interest rates and fees, lenders can generate substantial income.

However, profitability depends on effective risk management, as default rates can be high. Strict regulation compliance and proper borrower screening are vital to maintaining long-term profitability.

2. What is the minimum capital for a lending company in the Philippines?

The Securities and Exchange Commission (SEC) mandates that a lending company in the Philippines have a minimum capital requirement of PHP 1 million.

This ensures that companies have sufficient funds to operate and meet regulatory standards. However, lending firms may need more capital depending on the scale of their operations and the types of loans they provide.

3. Can a foreigner own a lending company in the Philippines?

Yes, a foreigner can own a lending company in the Philippines, but foreign ownership is limited to 40% as per the Foreign Investments Act. Filipino citizens or entities must own the remaining 60%.

Moreover, foreign investors must comply with local regulations, including SEC registration and capital requirements, to operate a lending business legally in the country.

4. How do I get a lending license in the Philippines?

To get a lending license in the Philippines, follow these steps -

- Register the company with the SEC.

- Submit required documents, including Articles of Incorporation and financial statements.

- Comply with a minimum capital of PHP 1 million.

- Obtain a Certificate of Authority from the SEC.

- Pay necessary fees and complete compliance with local regulations.