What drives the growth of digital banks in the Philippines, and can they achieve sustainable profitability in a competitive market? Nonbank financial institutions (NBFIs) in the Philippines are crucial players in the country's financial ecosystem, offering a wide range of services that go far beyond traditional banking solutions.

These institutions, including insurance companies, pawnshops, and microfinance firms, help diversify financial services, promote inclusion, and stabilize the economy. However, many still come across the challenge of distinguishing the unique operational frameworks and services provided by NBFIs as opposed to traditional banking entities.

Therefore, to know what NBFIs in the Philippines are all about, in this blog, we will provide insights into the various types of NBFIs operating in the Philippines today, their significant impact on the nation’s financial system, and the regulatory frameworks that govern them.

What Are Nonbank Financial Institutions in The Philippines?

Nonbank financial institutions (NBFIs) are entities that provide financial services but do not have a full banking license. In the Philippines, NBFIs play a significant role in expanding access to financial products, particularly for underserved segments of the population.

Essentially, they complement the formal banking sector by offering specialized services and products that banks typically do not provide. Here, take a look at some of its key features below:

1. Diverse Financial Services

NBFIs offer a wide range of services such as insurance, leasing, microfinance, remittances, pawnshop services, and investment management. They cater to both retail and institutional clients and often fill gaps left by traditional banks.

2. Focus on Financial Inclusion

Many NBFIs, particularly microfinance institutions and pawnshops, focus on serving low-income households and small businesses. Their services are crucial in promoting financial inclusion, especially in rural areas where banks may not have a strong presence.

3. Regulated by the BSP and Other Agencies

While NBFIs are not governed by the same regulations as banks, they are still subject to oversight by various regulatory bodies. The Bangko Sentral ng Pilipinas (BSP) supervises certain types of NBFIs, while other agencies like the Insurance Commission or the Securities and Exchange Commission (SEC) regulate other sectors like insurance and investment firms.

4. Flexible Loan and Credit Products

NBFIs often provide alternative credit products that may be more accessible to individuals or businesses with limited access to traditional bank loans. These include microloans, salary loans, and pawnshop loans, which have fewer strict requirements than bank loans.

5. Higher Risk and Interest Rates

Due to their higher risk profiles and fewer strict regulatory oversight, NBFIs often charge higher interest rates compared to banks. This reflects the additional risks they take by lending to clients with limited credit histories or financial stability.

6. Quick Access and Convenience

NBFIs, particularly pawnshops and microfinance institutions, provide quick and convenient access to financial services. For example, pawnshops offer instant loans with minimal documentation, while mobile money services allow for fast and secure money transfers.

7. Investment Opportunities

NBFIs also offer investment products such as mutual funds, unit investment trust funds (UITFs), and insurance policies. These products provide individuals with opportunities to grow their wealth outside of traditional banking channels.

Also Read: Using a Checklist Before Taking Out a Personal Loan in The Philippines

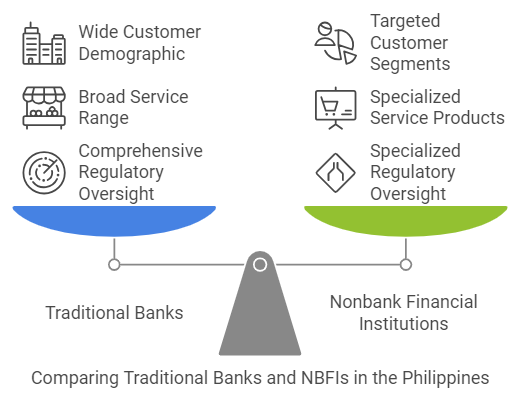

Traditional Banks Vs. Nonbank Financial Institutions in The Philippines - Key Differences Between Them

Both traditional banks and NBFIs play essential roles in the financial system, but they operate under different frameworks and offer distinct services. While banks focus on comprehensive financial services, NBFIs specialize in targeted financial products, often catering to specific market needs.

Here, take a closer look at the key differences between the two:

1. Regulatory Oversight

Traditional banks are heavily regulated by the Bangko Sentral ng Pilipinas (BSP) under the Banking Law, which sets strict requirements regarding capitalization, reserve funds, lending, and other banking operations.

In contrast, NBFIs, while also regulated by the BSP and other agencies like the Insurance Commission (IC) or the Securities and Exchange Commission (SEC), are subject to less comprehensive oversight, depending on their nature.

2. Range of Services

Traditional banks provide a broad spectrum of services, including savings and checking accounts, loans, credit cards, remittances, and investment products. These services are tailored to both retail and business clients.

In contrast, NBFIs focus on specialized financial products, such as microfinance, leasing, insurance, and pawnshop services.

3. Customer Base

Banks generally cater to a wide demographic, including individuals, corporations, and the government. Their offerings are designed to meet the needs of more financially established customers.

NBFIs, however, often target underserved groups, such as low-income households, micro-entrepreneurs, or people with limited access to formal banking services.

4. Capitalization and Requirements

Banks are required to maintain higher capital reserves compared to NBFIs to ensure they can cover potential risks. This makes them more stable and able to offer larger loans and a greater variety of financial products.

NBFIs, on the other hand, typically operate with lower capital requirements, which can allow for faster decision-making and more flexible products. However, this also means that NBFIs might not have the same capacity for large-scale lending as banks.

5. Access to Credit and Loan Terms

One of the most significant differences is the type of credit and loan products offered. Banks provide a wide array of loan products with relatively lower interest rates due to their larger financial reserves and more established customer base.

In contrast, NBFIs, particularly microfinance institutions, and pawnshops, offer more accessible credit products with quicker approval processes and less strict documentation, but often with higher interest rates.

6. Technology and Convenience

While traditional banks have embraced digital banking, many NBFIs, such as pawnshops and micro-lenders, often operate on a more traditional, offline model. However, this is changing, as digital NBFIs are emerging, offering mobile-based loan applications and financial services.

Banks, especially digital banks in the Philippines, offer a seamless online experience for everything from applying for loans to managing accounts. This makes traditional banks, particularly digital-first ones, more convenient for tech-savvy customers.

7. Risk and Interest Rates

Due to their more rigorous regulatory requirements and financial stability, banks typically offer lower interest rates on loans compared to NBFIs. This is because banks have more resources and can spread the risk of lending over a larger portfolio.

On the other hand, NBFIs often charge higher interest rates as they cater to high-risk clients, such as individuals with poor credit histories or businesses with limited financial backing.

Do you need more clarity regarding traditional banks and non-bank financial institutions operating in the Philippines? Check out this video. It explains in detail what these two financial options actually are and explores the core differences between them.

Also Read: Fighting Loan Shark Harassment in the Philippines

Ready to grow your Philippine SME? Apply now for N90’s fast financing solutions and get the funds you need to realize your business dreams! Get potential loan approvals within 24 hours to propel your business to new heights and reach new milestones.

Types of Nonbank Financial Institutions Operating in The Philippines

NBFIs play a crucial role in the Philippines’ financial system by offering a range of services without the need to hold a traditional banking license. Unlike banks, these entities are not bound by the same regulations, allowing them to provide specialized services.

Here, check out the different types of NBFIs operating in the Philippines:

1. Microfinance Institutions (MFIs)

Microfinance institutions are specialized NBFIs that provide small loans, savings products, and insurance services to low-income individuals and micro-entrepreneurs who do not have access to traditional banking services.

2. Pawnshops

Pawnshops are nonbank financial institutions that provide short-term loans to individuals in exchange for valuable personal items such as jewelry, electronics, and other assets.

3. Leasing Companies

Leasing companies in the Philippines provide financing solutions for businesses and individuals looking to acquire property, vehicles, or equipment through lease agreements. These institutions offer both operating and finance leases, enabling clients to use the assets without the need for upfront capital outlay.

4. Insurance Companies

Insurance companies are NBFIs that provide various types of insurance products, such as life, health, property, and casualty insurance. These institutions help individuals and businesses manage risks by offering protection against financial losses.

5. Investment Houses

Investment houses are financial institutions that specialize in investment services, including underwriting and selling securities, as well as providing financial advisory and wealth management services. They play an essential role in capital markets by assisting corporations in raising funds through public offerings and other investment vehicles.

6. Finance Companies

Finance companies offer a wide range of services, including personal loans, car loans, and small business financing. They typically provide loans to individuals and businesses that may not qualify for credit from traditional banks. These companies often have more flexible terms but may charge higher interest rates compared to banks.

7. Credit Cooperatives

Credit cooperatives are member-owned financial organizations that provide credit and savings services to their members. These cooperatives pool the savings of their members and offer loans at lower interest rates than traditional banks.

8. Crowdfunding Platforms

Crowdfunding platforms are online NBFIs that connect individuals or businesses with potential investors or lenders to fund specific projects or ventures. These platforms enable them to raise capital for various purposes, including startups, community projects, and personal needs.

9. Investment Banks

Investment banks in the Philippines focus on corporate finance activities such as mergers and acquisitions, investment advisory, and underwriting securities. They assist businesses in raising capital through the issuance of stocks, bonds, or other financial instruments.

10. Trust Entities

Trust entities, which include trust companies and banks offering trust services, act as trustees in managing assets on behalf of individuals, corporations, or other institutions. These entities provide services such as estate planning, asset management, and trust fund management.

Also Read: Dangers of Online Loan Apps in The Philippines

Role of Nonbank Financial Institutions in the Philippines’ Financial System

NBFIs fill critical gaps in the Philippines’ financial ecosystem, offering services traditional banks may not provide. Here, take a look at the role they play in contributing to the country’s overall financial ecosystem:

1. Promoting Financial Inclusion

NBFIs help promote financial inclusion by offering services to individuals and businesses that may not have access to traditional banks. For instance, microfinance institutions (MFIs) provide small loans to low-income individuals, while pawnshops offer quick, collateral-based loans.

2. Supporting SMEs

Nonbank financial institutions, such as leasing companies and finance companies, play a critical role in supporting the growth of SMEs in the Philippines. They provide financing options for businesses that may not meet the stringent requirements of traditional banks.

3. Providing Alternative Financing Sources

NBFIs serve as an important source of alternative financing for both individuals and businesses. For example, crowdfunding platforms offer a way for individuals or startups to raise capital without relying on traditional loans from banks.

4. Enabling Risk Management

Insurance companies, as a key type of NBFI, help individuals and businesses manage financial risks. By offering a range of insurance products, such as life, health, and property insurance, they provide a safety net against unexpected events, which is vital for financial security.

5. Enhancing Capital Market Efficiency

Investment banks and other related NBFIs enable the efficient functioning of capital markets by providing investment advisory, underwriting, and securities trading services. They essentially help businesses raise capital through stock and bond issuance, thereby promoting economic growth.

6. Offering Specialized Financial Products

NBFIs offer specialized financial products that cater to specific needs not addressed by traditional banks. For example, trust companies provide estate planning and asset management services, while pawnshops offer short-term, collateral-based loans.

7. Contributing to Economic Stability

Nonbank financial institutions contribute to the stability of the financial system by providing diversified financial services. By offering alternative financing and risk management options, NBFIs help stabilize the economy during financial crises or downturns.

8. Encouraging Investment in the Economy

NBFIs such as insurance companies and investment houses encourage investment in various sectors, including real estate, infrastructure, and stocks. By offering investment products and services, they direct capital toward productive sectors of the economy, which can lead to job creation and increased economic activity.

9. Filling Gaps in the Lending Market

Nonbank financial institutions help address gaps in the lending market by offering credit products that traditional banks may not provide, particularly for underserved populations.

Through accessible loan products like micro-loans, pawnshop loans, and payday loans, NBFIs help individuals and businesses gain access to credit, influence local economies, and improve livelihoods.

Also Read: How Do Interest Rates Work in The Philippines, And What Are Their Types

Regulatory Framework For Nonbank Financial Institutions in The Philippines

NBFIs in the Philippines are vital to the country’s financial ecosystem, offering a range of services from microloans to insurance products. However, their operations are closely regulated to ensure consumer protection, financial stability, and the proper functioning of the financial system.

Here, take a look at the regulatory framework NBFIs must follow to operate legally and efficiently in the Philippines:

1. The Securities and Exchange Commission (SEC)

The SEC is the primary regulatory body overseeing many NBFIs in the Philippines. It regulates institutions like investment houses, financing companies, and leasing companies. The SEC ensures that these entities comply with the rules governing corporate governance, financial transparency, and consumer protection.

2. The Bangko Sentral ng Pilipinas (BSP)

The BSP plays a key role in regulating certain types of NBFIs, particularly those engaged in lending and microfinance. It oversees the operations of pawnshops, remittance companies, and microfinance institutions (MFIs) to ensure they adhere to financial standards and comply with anti-money laundering (AML) regulations.

3. The Insurance Commission (IC)

Nonbank financial institutions offering insurance services are regulated by the Insurance Commission (IC), which supervises the insurance industry in the Philippines. The IC ensures that insurance companies, mutual benefit associations, and pre-need companies operate in a financially sound manner.

4. The Department of Trade and Industry (DTI)

The Department of Trade and Industry (DTI) is responsible for regulating NBFIs involved in consumer protection, especially those that offer credit products, like pawnshops and lending companies. The DTI enforces consumer protection laws and ensures that NBFIs comply with fair lending practices.

5. The Anti-Money Laundering Council (AMLC)

The AMLC plays a crucial role in regulating NBFIs in terms of preventing money laundering and other illicit financial activities. Nonbank financial institutions must adhere to stringent Anti-Money Laundering (AML) laws, ensuring that their operations are transparent and that they do not encourage or enable the movement of illicit funds.

6. The Philippine Deposit Insurance Corporation (PDIC)

For NBFIs that offer deposit-like services, such as savings accounts or investment products, the Philippine Deposit Insurance Corporation (PDIC) provides a safety net by insuring deposits up to a certain amount. The PDIC’s oversight aims to protect depositors in case of insolvency or failure of a financial institution.

7. Regulatory Compliance with Capital and Risk Management Standards

NBFIs must meet specific capital adequacy requirements and implement robust risk management frameworks. These measures are essential to ensure financial stability and protect consumers from over-indebtedness.

Regulatory bodies like the SEC and BSP impose rules regarding the minimum capital requirements and risk management practices that NBFIs must adopt to operate safely within the financial system.

8. Consumer Protection Laws

Consumer protection is a key component of the regulatory framework for NBFIs in the Philippines. The government has established laws to protect consumers from abusive practices, such as unfair interest rates, hidden fees, or predatory lending.

The DTI and BSP are responsible for ensuring that NBFIs comply with these laws and that consumers have access to transparent information about the terms and conditions of financial products.

9. Licensing and Registration Requirements

Before they can begin operations, nonbank financial institutions must obtain the necessary licenses and registrations from the relevant regulatory authorities. Depending on the type of NBFI, this could involve registration with the SEC, BSP, or the IC.

10. Enforcement and Penalties

Regulatory bodies such as the SEC, BSP, and IC are responsible for enforcing the rules and regulations governing NBFIs. These agencies have the authority to impose penalties, sanctions, and fines on institutions that violate the rules.

Enforcement actions could include revoking licenses, imposing financial penalties, or taking legal action against NBFIs involved in fraudulent or illegal activities. This ensures accountability and deters misconduct within the industry.

Also Read: Notarized Loan Agreement in the Philippines: A Sample Contract

Challenges Faced by Nonbank Financial Institutions When Operating in Philippines

As NBFIs continue to grow and gain significance in the financial landscape, they encounter various challenges that they must navigate effectively to sustain their operations and competitiveness.

Here, take a look at the challenges both policymakers and industry players need to be aware of to ensure NBFIs can operate effectively in the Philippines:

1. Regulatory Compliance and Legal Constraints

Nonbank financial institutions are subject to strict regulatory oversight by multiple government agencies, such as the Bangko Sentral ng Pilipinas (BSP), the Securities and Exchange Commission (SEC), and the Insurance Commission (IC). Complying with these regulations can be potentially time-consuming and costly.

2. Limited Access to Capital

Many NBFIs struggle with limited access to capital, especially when compared to traditional banks. Since they are not part of the formal banking system, they often face higher costs of funding and stricter lending conditions when borrowing from commercial banks or other financial institutions.

3. Consumer Trust and Perception

Despite offering valuable financial products, NBFIs sometimes face challenges in earning consumer trust. Negative perceptions around fees, interest rates, and lack of transparency often create skepticism.

4. Operational and Technological Challenges

The rapid growth of digital financial services in the Philippines requires NBFIs to adopt and integrate advanced technology into their operations. However, many NBFIs struggle with limited technological infrastructure and cybersecurity capabilities.

5. Competition from Traditional Banks and Fintech Startups

NBFIs face stiff competition not only from traditional banks but also from fintech startups offering innovative solutions. Banks, with their extensive financial resources and established consumer base, can offer more competitive rates and products.

6. Risk Management and Credit Risk

Effective risk management is critical for the long-term success of NBFIs. However, many institutions face challenges in managing credit risk, especially in a market with high levels of non-performing loans.

7. Lack of Financial Literacy Among Borrowers

Many customers of NBFIs in the Philippines have limited financial literacy. This can result in poor decision-making when it comes to loan repayment, insurance policies, or investment products.

8. Limited Market Reach in Rural Areas

While NBFIs provide much-needed financial services to the underbanked and underserved populations in urban areas, reaching customers in rural and remote areas remains a challenge.

9. Economic Volatility and Market Fluctuations

The Philippine economy is subject to fluctuations, which can impact the financial stability of NBFIs. Changes in interest rates, inflation, or currency devaluation can negatively affect the lending business or the performance of investment products.

10. Data Privacy and Security Concerns

As more NBFIs adopt digital platforms for delivering financial services, data privacy and cybersecurity become significant concerns. There are risks associated with storing and processing sensitive customer information, which could be targeted by cybercriminals.

Conclusion

NBFIs play a pivotal role in enhancing financial inclusion and supporting the stability of the Philippine financial system. By providing alternative financial products such as loans, insurance, and investment options, they serve underbanked populations and offer diversified financial services.

Additionally, while they face challenges like regulatory compliance, limited access to capital, and competition from traditional banks, their adaptability and innovation contribute to a more resilient financial ecosystem. As digital solutions and financial technologies continue to evolve, NBFIs are positioned to further support the Philippines’ economic growth and financial stability.

Moreover, to thrive in an increasingly competitive environment, NBFIs need to address key challenges, maintain consumer trust, and stay aligned with evolving regulations. With the right strategies, NBFIs will continue to play a vital role in providing individuals and businesses in the Philippines with accessible financial solutions.