Signing a small business loan agreement in the Philippines is a significant step that could impact your business's future, still, many aspiring Filipino entrepreneurs like you are overwhelmed by the complex terms and conditions they encounter in these agreements.

Therefore, understanding these details is crucial, as it will prevent you from making costly mistakes, such as ignoring hidden fees, and not properly assessing their repayment capabilities, to ensure an overall favorable loan borrowing experience.

So, to set you up for success, in this blog, we will guide you through the various sections of a loan agreement, from understanding the key components and legal considerations to navigating the fine print and identifying potential red flags.

It is fair to say that by the end of this detailed article, you will be well-equipped with all the knowledge to make sound financial decisions when entering into a small business loan agreement in the Philippines. So, without any more delays, let us jump into all the details worth exploring.

What is a Small Business Loan Agreement in The Philippines?

A Small Business Loan Agreement in the Philippines is a legally binding contract between a lender, such as a bank, government agency, or private institution, and a small business borrower.

It essentially outlines the loan amount, interest rate, repayment terms, collateral (if any), and conditions under which the loan is granted. This agreement protects both parties by clearly specifying the obligations and rights regarding the loan.

Also Read: How Do Interest Rates Work in The Philippines, And What Are Their Types

Critical Components of a Small Business Loan Agreement in the Philippines

When considering taking on a small business loan in the Philippines, it’s crucial to understand the main components of the small business loan agreement.

Here are a few prominent components of a small business loan agreement in the Philippines -

1. Loan Amount: Specifies the total amount borrowed by the business, including any disbursement terms.

2. Interest Rate: Defines the rate charged on the loan, whether fixed or variable, and the calculation method.

3. Repayment Terms: Outlines the schedule, amount, and duration of loan repayment, including any grace periods.

4. Collateral: Describes the assets pledged as security for the loan, if applicable, and the conditions for their forfeiture.

5. Default Provisions: Specifies the consequences and actions taken if the borrower fails to meet repayment obligations.

6. Prepayment Terms: States whether early repayment is allowed and if penalties apply.

7. Loan Purpose: Clearly define the loan's intended use, ensuring it aligns with business operations.

8. Fees and Charges: Lists all additional costs, including processing fees, late charges, and penalties for non-compliance.

9. Governing Law: Indicates the agreement's legal framework, typically following Philippine law.

10. Signatures and Execution: This process confirms the parties' agreement to the terms through authorized signatures from both the borrower and lender.

Also Read: Getting Emergency Loans Online in the Philippines: Tips and Options

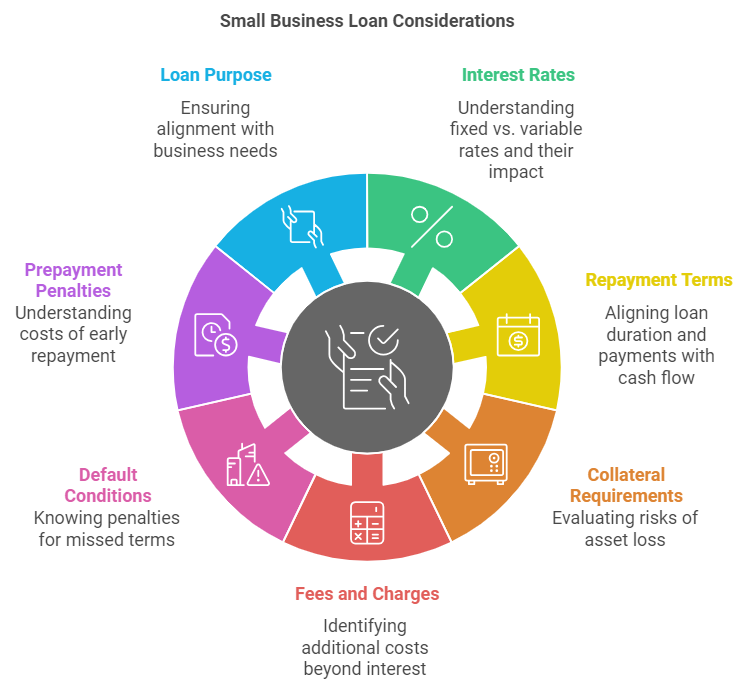

Crucial Aspects To Know About Before Signing a Small Business Loan Agreement in The Philippines

Before signing a small business loan agreement, it's crucial to thoroughly understand the terms and conditions to ensure the loan benefits your business without causing financial strain.

Here are vital factors to consider before signing a small business loan agreement in the Philippines -

1. Interest Rates

Understanding the interest rate is essential, as it affects the total cost of the loan. Check whether the rate is fixed or variable, as variable rates can fluctuate, impacting your monthly payments.

A lower interest rate may reduce your financial burden but ensure you know of any hidden fees that could increase the cost.

2. Repayment Terms

Review the repayment schedule carefully, including the loan duration and monthly payments. Make sure it aligns with your business cash flow.

If the payments are too high or the schedule too tight, it could strain your operations. Some loans may offer grace periods or flexible terms, which can be beneficial.

3. Collateral Requirements

Some loans require collateral, such as property or equipment, to secure the loan, so before agreeing to a loan, evaluate the risk of losing these assets if you cannot repay them.

Ensure you fully understand the lender’s collateral requirements and the potential consequences of defaulting on the loan.

4. Fees and Charges

Beyond the interest, loans may come with additional fees like processing, prepayment, or late payment charges. Be transparent about all associated costs before signing.

These extra fees can add up over time, making the overall loan more expensive than initially expected, so including them in your financial planning is essential.

5. Default Conditions

Knowing what constitutes a default is crucial, as failure to meet certain terms can lead to severe penalties, as these conditions may include reasons such as late payments or violating loan terms.

Getting to know the actual cause of the default helps you avoid costly consequences such as legal action or seizure of collateral down the road.

6. Prepayment Penalties

Some lenders charge fees for early repayment of the loan. If you plan to pay off your loan beforehand, ensure you understand any prepayment penalties.

Doing so helps you avoid unexpected costs and allows you to weigh the benefits of early repayment versus potential extra charges.

7. Loan Purpose

Ensure that the loan agreement clearly defines the purpose of the loan and that it aligns with your business needs. Misusing the loan for unauthorized purposes could lead to a breach of contract and penalties.

To know more about the criteria for applying for a small business loan, check out this video. It lists all the essential points businesses and individuals need to qualify for before applying for a small business loan.

Also Read: Top Lending Services in Cebu City, Philippines

Say goodbye to financial roadblocks. Apply for N90’s fast financing solutions today and give your Philippine SME the boost it deserves! Get potential loan approvals within 24 hours to finance your business and take it to the next level! Get in touch with us today!

Types of Small Business Loan Agreements Available in The Philippines

In the Philippines, various small business loan agreements cater to different needs of businesses and individuals. Each type of small business loan agreement has its own set of terms, conditions, and purposes, offering flexibility based on the borrower's requirements.

Here are the common types of small business loan agreements available in the Philippines for businesses and individuals alike -

1. Term Loan Agreement

A fixed amount is borrowed and repaid over a specified period with regular payments. Ideal for business expansion, capital expenditures, or long-term investments.

2. Revolving Credit Agreement

Borrowers have access to a set credit limit they can draw from repeatedly, repaying only the used amount. It provides flexibility for managing short-term cash flow needs.

3. Secured Loan Agreement

The borrower must pledge collateral, such as property or assets, to secure the loan. Typically offers lower interest rates but comes with the risk of losing the collateral in case of default.

4. Unsecured Loan Agreement

No collateral is required, but the borrower may face higher interest rates due to increased risk for the lender. This type of agreement is often used for personal loans or small business loans.

5. Bridge Loan Agreement

Short-term financing is used to bridge gaps in cash flow, often during a transition or until long-term financing is secured. These loans usually have higher interest rates and shorter repayment periods.

6. Microfinance Loan Agreement

Designed to support small businesses and entrepreneurs, especially those in low-income areas. Microfinance loans typically have lower amounts and shorter repayment terms.

7. Trade Finance Loan Agreement

This type of agreement is used mostly for international or domestic trade transactions, helping businesses fund purchases of goods and services. This type of loan agreement is critical for importers and exporters.

Also Read: Understanding the Role and Importance of MSME in The Philippine Economy

Legal Considerations and Regulations To Know Before Signing a Small Business Loan Agreement in the Philippines

Before signing a small business loan agreement in the Philippines, it's essential to understand the legal considerations and regulations that protect both the borrower and lender. Compliance with these laws ensures fair practices and avoids legal complications.

Here are some of the crucial legal aspects for small business owners to consider before signing a small business loan agreement in the Philippines -

1. Securities and Exchange Commission (SEC) Registration

Ensure that the lending institution is registered with the SEC and has the necessary licenses, particularly the Certificate of Authority, to operate

2. Lending Company Regulation Act of 2007

This law regulates lending practices, ensuring fair terms and preventing predatory lending. Borrowers should check that their agreement complies with this law.

3. Truth in Lending Act

Lenders must fully disclose all loan terms, including interest rates, fees, and repayment schedules, to ensure transparency and protect borrowers from hidden charges.

4. BSP Regulations

The Bangko Sentral ng Pilipinas (BSP) regulates bank and financial institution loans, ensuring that interest rates and fees adhere to legal limits.

5. Data Privacy Act

Lending companies must comply with data privacy laws and safeguard personal and financial information shared during the loan application process.

6. Contract Terms and Conditions

Review all terms in the loan agreement, including interest rates, repayment schedules, collateral, and default conditions, to ensure they are legally binding and reasonable.

7. Debt Collection Practices

Borrowers should be aware of legal debt collection practices under Philippine law, which protect them from harassment and unethical collection methods.

Also Read: Best Medical Practice Loans For Physicians in The Philippines

Final Steps Before Signing a Small Business Loan Agreement - Potential Tips to Use And Pitfalls to Avoid

Before signing a small business loan agreement, navigating the final steps carefully is essential to avoid costly mistakes and ensure the loan meets your business needs.

Here, take a look at some tips to successfully navigate through the process of signing a loan agreement in the Philippines -

Tips to Use

1. Read the Fine Print

Carefully review all terms, conditions, and clauses to fully understand the interest rates, fees, repayment schedules, and penalties before committing.

2. Seek Legal Advice

Consider consulting with a lawyer or financial advisor to ensure the agreement is fair and compliant with the law. Professional guidance can help clarify any legal jargon.

3. Clarify Loan Purpose and Use

Ensure the loan purpose aligns with your business goals, and clarify any restrictions on how the funds can be used to avoid breaching the agreement.

4. Negotiate Terms

Don't hesitate to negotiate better terms, such as lower interest rates, longer repayment periods, or more flexible conditions that fit your business’s financial situation.

5. Request Written Confirmation

To avoid misunderstandings, obtain all verbal promises from the lender in writing. Any agreed-upon changes should be documented in the contract.

Now that we know about the tips, let us now shed some light on the potential pitfalls business owners need to avoid before signing a small business loan agreement -

Also Read: Guide to Best Restaurant Business Loans for Small Businesses in 2024

Potential Pitfalls to Avoid

1. Ignoring Hidden Fees

Overlooking additional charges like processing fees or penalties can lead to unexpected costs. Ensure all fees are transparent and factored into your final decision.

2. Rushing the Process

Avoid signing in haste without fully understanding the implications of the loan terms. Take your time to evaluate whether the loan is essential for your business.

3. Not Assessing Repayment Ability

Failure to assess your ability to meet the repayment terms can lead to default and financial strain. Make sure your business cash flow can accommodate the repayments.

4. Over-Borrowing

Taking out a loan larger than necessary can create an unnecessary financial burden. Only borrow what your business can effectively manage and repay.

Conclusion

As this article has explained in great detail, being well-informed before signing a small business loan agreement in the Philippines is important, as it allows businesses and individuals to make the right financial decisions that will significantly impact their long-term success and growth.

One of the best ways to approach this is by understanding your financial standing, maintaining a strong credit profile, clearly defining the purpose of your loan, and monitoring market conditions. Ensuring all loan terms are clear and beneficial is crucial to avoid future complications.

If needed, dive deeper into the nuances of the loan agreement to better understand the repayment timeline, interest rates, and any potential penalties. This proactive approach will eliminate the chances of unwelcome surprises springing up unnoticed down the road.

Additionally, your commitment to preparing a comprehensive loan proposal and business plan also plays a key role in securing beneficial terms. Doing so demonstrates your sincere dedication and readiness to potential lenders, improving your overall chances of getting your loan approved and receiving favorable terms.

Frequently Asked Questions (FAQs)

1. When signing a loan agreement, what should you make sure of?

When signing a loan agreement in the Philippines, make sure of the following points -

- Get a clear understanding of interest rates and repayment terms.

- All fees and charges are transparent.

- Loan purpose aligns with your business goals.

- Collateral and penalties are clearly defined.

- Legal compliance with local regulations.

- Get everything in writing including verbal agreements or changes.

2. Do loan agreements need to be notarized in the Philippines?

No, loan agreements do not always need to be notarized in the Philippines to be legally binding. However, notarization adds an extra layer of authenticity and ensures that the document was signed voluntarily.

Moreover, it also agrees a public document, which can be beneficial in case of disputes or legal enforcement. It's often recommended for larger or more formal loans.

3. What are 5 pieces of information you need to apply for a loan in the Philippines?

To apply for a loan in the Philippines, you typically need the following information -

- Valid ID for personal identification.

- Proof of income such as payslips or financial statements.

- Business registration documents (for business loans).

- Collateral details (if required).

- Loan purpose outlining how the funds will be used.

4. What is the maximum interest rate allowed for a loan by law in the Philippines?

In the Philippines, the Bangko Sentral ng Pilipinas (BSP) has capped the maximum interest rate for loans at 6% per month or 0.5% per day for consumer loans like payday loans, under Circular No. 1133.

This regulation aims to protect borrowers from excessively high interest rates, especially for short-term loans from non-bank lenders.